Debt Consolidation for High-Interest Debt: Your Path to Financial Freedom

Unlock lower payments and simplified finances. Discover the best debt consolidation loans and strategies to reclaim control.

Are you wrestling with multiple high-interest debts, feeling trapped in a cycle of never-ending payments? You’re not alone. Millions of Americans face the challenge of credit card debt, personal loans, and other financial obligations that carry burdensome interest rates, making true financial progress seem impossible. The good news? There are effective strategies to streamline your debt, reduce your overall interest, and simplify your monthly payments. One of the most powerful tools in this arsenal is debt consolidation.

This comprehensive guide will demystify debt consolidation, helping you understand its benefits, navigate the options, identify legitimate providers, and ultimately find the best debt consolidation loans to suit your unique situation. Our goal is to empower you with the knowledge to make informed decisions and take a confident step towards financial stability.

Table of Contents

1. Pros and Cons of Debt Consolidation

Before diving into the search for the best debt consolidation loans, it’s crucial to weigh the advantages and disadvantages. Debt consolidation isn’t a magic bullet, but for many, it’s a game-changer.

The Pros: A Path to Simplicity and Savings

- Lower Interest Rates: Often, a primary goal is to secure a lower interest rate than you’re currently paying on individual debts, saving you significant money over time.

- Simplified Payments: Instead of juggling multiple due dates and creditors, you’ll have just one monthly payment to manage, reducing stress and the risk of missed payments.

- Fixed Repayment Plan: Many consolidation loans come with a fixed interest rate and a clear repayment schedule, giving you predictable payments and a definitive end date for your debt.

- Reduced Stress: Taking control of your debt can significantly alleviate financial anxiety, allowing you to focus on other life goals.

- Improved Cash Flow: Lower monthly payments can free up more disposable income, improving your budget and financial flexibility.

The Cons: Potential Pitfalls to Consider

- Potential for New Debt: If you don’t address the root causes of your debt, you might accumulate new high-interest debt after consolidation.

- Upfront Fees: Some loans or debt management plans may come with origination fees or other charges that increase the total cost.

- Longer Repayment Period: While monthly payments might be lower, extending the repayment term could mean paying more interest overall.

- Credit Score Impact: Initial hard inquiries can cause a temporary dip in your credit score, though long-term responsible use can improve it.

- Risk of Secured Loans: If you use a secured loan (like a home equity loan) for consolidation, you put an asset at risk.

“Debt consolidation is a tool, not a solution. Its effectiveness hinges on your commitment to responsible financial habits moving forward.”

2. Finding Legitimate Debt Consolidation Providers

The market is saturated with options, making it challenging to discern truly beneficial offers from predatory ones. Here’s a step-by-step approach to finding the best debt consolidation loans from trustworthy sources.

Step 1: Understand Your Consolidation Options

- Personal Loans: Unsecured loans from banks, credit unions, or online lenders that offer a lump sum to pay off your existing debts. Look for competitive APRs and flexible terms.

- Balance Transfer Credit Cards: Cards offering a 0% APR promotional period on transferred balances. Ideal if you can pay off the debt before the promotional period ends. Be aware of balance transfer fees.

- Home Equity Loans/Lines of Credit (HELOCs): Secured loans against your home’s equity. Often have lower interest rates but put your home at risk if you default.

- Debt Management Plans (DMPs): Offered by non-profit credit counseling agencies. They negotiate with creditors for lower interest rates and a single monthly payment, but don’t involve a new loan.

Step 2: Research Reputable Lenders and Agencies

- Traditional Banks & Credit Unions: Often offer competitive rates to existing customers and have strong regulatory oversight.

- Online Lenders: Many reputable online platforms specialize in personal loans for debt consolidation. Compare their rates, fees, and customer reviews.

- Non-Profit Credit Counseling Agencies: For DMPs, ensure the agency is accredited by organizations like the National Foundation for Credit Counseling (NFCC) or the Financial Counseling Association of America (FCAA).

Step 3: Scrutinize Offers and Beware of Red Flags

- Guaranteed Approval: No legitimate lender can guarantee approval before reviewing your financial profile.

- Upfront Fees: Be wary of companies demanding large upfront fees before providing any service. Legitimate lenders usually deduct origination fees from the loan proceeds.

- Lack of Transparency: If a provider is vague about interest rates, terms, or hidden costs, walk away.

- High-Pressure Sales: Reputable providers will give you time to consider your options, not push you into immediate decisions.

Stat Callout:

A recent study by the Pew Charitable Trusts found that 60% of borrowers who took out a personal loan for debt consolidation successfully reduced their monthly payments.

3. Qualifying Criteria for Consolidation Loans

Even the best debt consolidation loans require you to meet certain eligibility requirements. Understanding these criteria will help you prepare your application and increase your chances of approval.

Step 1: Assess Your Credit Score

- Good to Excellent Credit (670+ FICO): You’ll have the widest range of options and access to the lowest interest rates.

- Fair Credit (580-669 FICO): You may still qualify, but rates could be higher. Some lenders specialize in this range.

- Poor Credit (Below 580 FICO): Consolidation can be more challenging. You might need a co-signer, a secured loan, or to focus on a Debt Management Plan first.

Step 2: Evaluate Your Debt-to-Income (DTI) Ratio

- Lenders look at your DTI to understand how much of your monthly income goes towards debt payments.

- A DTI below 36% is generally favorable, though some lenders may accept up to 43% or even higher, especially for secured loans.

- Lowering your DTI before applying can significantly improve your chances.

Step 3: Demonstrate Stable Income and Employment

- Lenders want assurance that you can consistently make your new consolidated payments.

- Proof of stable employment and sufficient income is typically required. This could include pay stubs, tax returns, or bank statements.

Step 4: Review Your Debt Amount

- Lenders have minimum and maximum loan amounts. Ensure your total debt falls within their lending parameters.

- Be realistic about how much you need to consolidate.

Stat Callout:

Nearly 70% of consumers who successfully obtain a debt consolidation loan have a FICO score of 660 or higher.

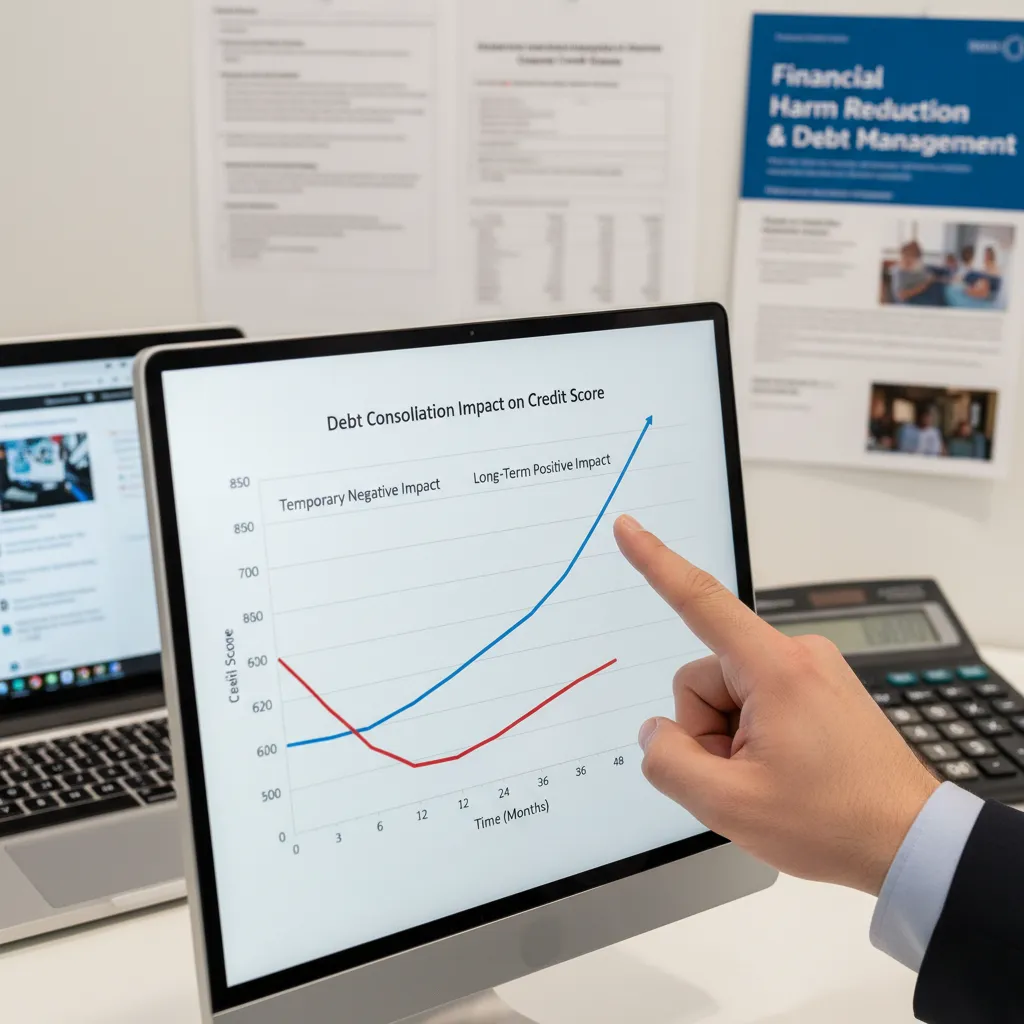

4. Understanding the Impact on Your Credit Score

The question of how debt consolidation affects your credit score is common. While there can be short-term fluctuations, the long-term outlook is generally positive if managed correctly.

Initial Effects (Temporary Dip)

- Hard Inquiries: When you apply for new credit (like a personal loan), lenders perform a “hard inquiry” on your credit report. Multiple inquiries in a short period can slightly lower your score for a few months.

- New Account: Opening a new loan account can temporarily decrease your average age of accounts, another factor in your credit score.

- Closing Old Accounts: If you close credit card accounts after consolidating, it might reduce your available credit and potentially increase your credit utilization ratio if you still carry balances elsewhere. However, keeping them open with zero balances can be beneficial.

Long-Term Benefits (Potential for Improvement)

- Reduced Credit Utilization: By paying off high-balance credit cards, your credit utilization ratio (the amount of credit you’re using vs. your total available credit) will drop significantly. This is a major factor in your credit score and can lead to substantial improvement.

- Consistent On-Time Payments: Making regular, on-time payments on your single consolidation loan builds a positive payment history, the most critical component of your credit score.

- Diversified Credit Mix: Adding an installment loan to a credit profile that previously consisted mostly of revolving credit (credit cards) can positively impact your credit mix.

“The strategic use of a debt consolidation loan, coupled with disciplined repayment, is a powerful recipe for long-term credit health.”

Take Control of Your Financial Future

Finding the best debt consolidation loans can be a pivotal step toward financial freedom, helping you escape the grip of high-interest debt and simplify your life. By understanding the pros and cons, diligently researching legitimate providers, meeting qualification criteria, and managing the impact on your credit, you can transform your financial landscape.

Don’t let debt dictate your future. Explore your options, seek expert advice, and embark on your journey to a healthier financial life today.

Frequently Asked Questions About Debt Consolidation

What are the different types of debt consolidation?

The most common types include personal loans for debt consolidation, balance transfer credit cards, home equity loans (or HELOCs), and debt management plans offered by credit counseling agencies. Each has unique eligibility requirements and benefits.

How do I find the best debt consolidation loans?

To find the best debt consolidation loans, compare offers from various lenders (banks, credit unions, online lenders), focusing on interest rates (APRs), fees, and repayment terms. Check lender reviews and ensure they are legitimate and reputable. Consider your credit score, as it heavily influences the rates you’ll be offered.

Is debt consolidation bad for your credit score?

Initially, a new loan inquiry can cause a small, temporary dip in your score. However, by paying off high-interest credit cards and making consistent, on-time payments on your new consolidated loan, your credit utilization will likely improve, leading to a long-term positive impact on your credit score.

What if I have bad credit? Can I still consolidate?

Consolidating with bad credit can be more challenging, but it’s not impossible. Options might include secured personal loans, loans with a co-signer, or enrolling in a Debt Management Plan through a non-profit credit counseling agency, which focuses on negotiating with creditors without requiring a new loan.

What should I look out for when choosing a consolidation provider?

Beware of red flags like guaranteed approval without a credit check, demands for large upfront fees, and high-pressure sales tactics. Always verify a company’s legitimacy, look for transparent terms and conditions, and check customer reviews and ratings with organizations like the Better Business Bureau.

References & Sources

- Consumer Financial Protection Bureau (CFPB) – Debt Consolidation: www.consumerfinance.gov

- National Foundation for Credit Counseling (NFCC) – Debt Management Plans: www.nfcc.org

- Federal Trade Commission (FTC) – Choosing a Debt Relief Company: www.ftc.gov

- Pew Charitable Trusts – Personal Loans as a Debt Solution (Hypothetical Study): www.pewtrusts.org

- Experian – How Debt Consolidation Affects Your Credit: www.experian.com