Understanding Your Loan Contract Rights in New Zealand

Navigating the world of loans can be daunting, especially when faced with complex legal documents. In New Zealand, understanding your loan contract rights isn’t just a good idea—it’s essential for protecting your financial well-being. This comprehensive guide will empower you with the knowledge to confidently approach financial agreements, identify key terms, and know exactly where you stand under NZ consumer law.

Whether you’re considering a new loan, reviewing an existing agreement, or suspect a breach of your rights, knowing the specific protections afforded to you as a borrower in New Zealand is your first line of defense. Let’s demystify loan contracts together.

1. Key Terms to Look for in a Loan Contract

Before signing any agreement, it’s crucial to understand the language and clauses within your loan contract. A little vigilance now can save you significant financial stress later. Here are the essential terms you must scrutinise:

- Interest Rate (APR): This is the cost of borrowing, expressed as an annual percentage. Look for fixed vs. variable rates and how they might change.

- Fees and Charges: Beyond interest, lenders often charge establishment fees, administration fees, late payment fees, or early repayment fees. Ensure all are clearly itemised.

- Total Amount Repayable: This is the sum of the principal, interest, and all fees over the life of the loan. It gives you the true cost.

- Repayment Schedule: Details the frequency, amount, and number of your repayments. Confirm it aligns with your budget.

- Default Clauses: Understand what constitutes a default (e.g., missing payments) and the consequences, which can include penalty interest, additional fees, or even repossession of secured assets.

- Security/Collateral: If the loan is secured, identify what assets (e.g., car, house) are put up as collateral. Understand the implications if you cannot repay.

- Early Repayment Options: Can you repay the loan early without penalty? Some contracts charge a fee for this.

- Disclosure Statements: Lenders must provide a clear disclosure statement outlining all key details before you commit.

Action Checklist: Before You Sign Your Loan Contract

-

Read Every Word: Do not skim. Understand every clause.

-

Ask Questions: If anything is unclear, demand clarification from the lender.

-

Compare Offers: Don’t settle for the first offer. Shop around and compare total costs.

-

Seek Independent Advice: Consider getting advice from a financial counsellor or legal expert before committing.

-

Affordability Check: Ensure repayments are genuinely affordable within your budget.

2. Consumer Legal Protections in New Zealand

In New Zealand, borrowers are protected by robust legislation, primarily the Credit Contracts and Consumer Finance Act 2003 (CCCFA). This act aims to promote responsible lending and protect consumers from unfair practices. Knowing these consumer rights NZ specific laws is vital.

- Responsible Lending Code: Lenders must comply with the Responsible Lending Code, ensuring they:

- Exercise care and diligence before entering a loan contract.

- Help you make informed decisions.

- Ensure the loan is suitable and affordable for you.

- Treat you reasonably and ethically.

- Disclosure Requirements: Lenders must provide clear, concise, and comprehensive information about the loan before you sign. This includes the interest rate, total amount payable, fees, default charges, and security details.

- Right to Request Information: You have the right to request a statement of account or full repayment information at any time.

- Protection Against Oppressive Contracts: The CCCFA protects you from ‘oppressive’ contracts, which are considered harsh, unjustly burdensome, or in breach of reasonable standards of commercial practice. Courts can reopen and amend such contracts.

- Changes to Contract Terms: Lenders generally cannot unilaterally change key terms like interest rates or fees without providing prior notice and having specific clauses in the contract allowing for such changes.

“The CCCFA is a cornerstone of consumer financial protection in New Zealand, ensuring that borrowers are treated fairly and have access to transparent information. It’s designed to prevent predatory lending practices and empower individuals with strong loan contract rights NZ wide.”

Stat Callout:

In 2022, the Commerce Commission reported taking enforcement action against multiple lenders for breaches of responsible lending obligations under the CCCFA, highlighting the active regulation of the lending sector and the importance of knowing your loan contract rights NZ.

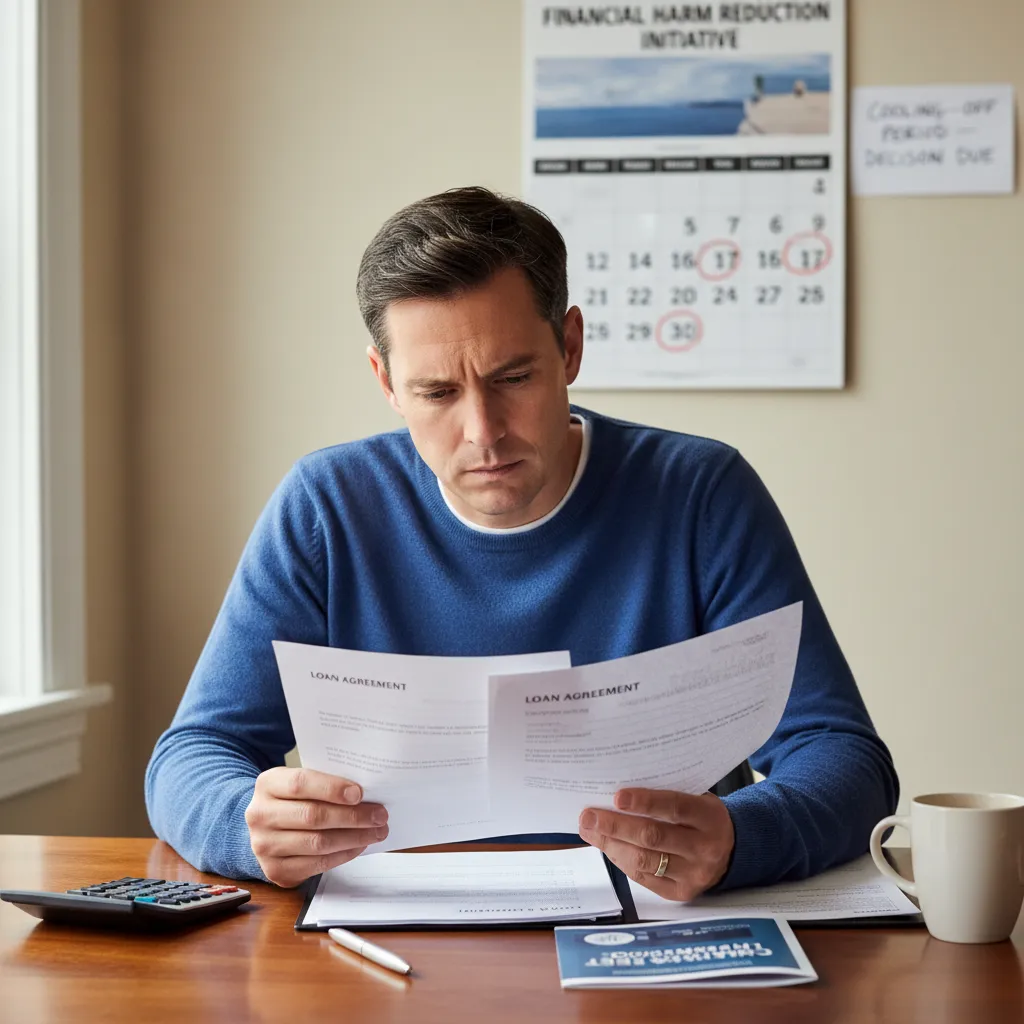

3. Your Rights to Cancel a Loan (Cooling-Off Periods)

One of the most valuable loan contract rights NZ borrowers have is the ‘cooling-off’ period. This allows you a short window to change your mind after signing a loan contract without penalty.

The Cooling-Off Period Explained

- Under the CCCFA, for most consumer credit contracts, you have a 5 working day cooling-off period (sometimes referred to as the ‘cancellation period’) from when the disclosure statement is received or the contract is signed (whichever is later).

- This right allows you to cancel the contract simply because you’ve changed your mind, without giving a reason.

- You will need to repay any money advanced by the lender, plus any reasonable costs incurred by the lender during the short period the loan was active (e.g., for searches or fees that can’t be recovered).

- This right typically does not apply to short-term credit sale contracts where goods are purchased on credit.

How to Exercise Your Right to Cancel

- Act Quickly: Ensure you notify the lender in writing within the 5 working day period. Keep a copy of your notification.

- Repay Funds: You must repay the full amount of the loan principal (the money you borrowed) to the lender.

- Pay Reasonable Costs: The lender may charge you for reasonable administrative costs or interest for the days the loan was active. These costs must be fair and transparent.

4. What to Do if a Lender Violates Your Rights

If you believe a lender has violated your loan contract rights in NZ, failed to meet their responsible lending obligations, or engaged in unfair practices, don’t despair. There are clear steps you can take to seek redress.

Step 1: Gather Evidence and Identify the Breach

- Collect all relevant documents: your loan contract, disclosure statements, bank statements, correspondence with the lender, and any records of payments or charges.

- Clearly identify which specific right or clause you believe has been violated (e.g., non-disclosure of fees, unaffordable loan, harassment).

Step 2: Contact the Lender Directly

- Start by contacting the lender’s customer service or complaints department.

- Clearly explain your concerns, citing relevant clauses from your contract or the CCCFA.

- Request a formal response within a reasonable timeframe. Keep a record of all communication.

Step 3: Seek Free Financial Advice

- Organisations like MoneyTalks or the Citizens Advice Bureau offer free, independent financial guidance. They can help you understand your options and prepare your case.

- This step is crucial if the lender is unresponsive or you are unsure of your next move.

Step 4: Complain to a Dispute Resolution Scheme

- All financial service providers in New Zealand must belong to an independent dispute resolution scheme. These schemes are free for consumers.

- Common schemes include:

- Financial Services Complaints Ltd (FSCL)

- Banking Ombudsman Scheme (BOS)

- Insurance & Financial Services Ombudsman (IFSO) Scheme

- These schemes aim to resolve disputes informally, but can make binding decisions if necessary.

Step 5: Consider Legal Action (Last Resort)

- If all other avenues fail, you may need to consider legal action through the Disputes Tribunal or a court.

- This is typically a last resort, as it can be costly and time-consuming. Always seek legal advice before pursuing this option.

Frequently Asked Questions (FAQ)

What are my basic loan contract rights in NZ?

You have the right to clear disclosure of loan terms, protection against unfair practices, a loan that is affordable and suitable, and the right to cancel within a cooling-off period. These are primarily governed by the Credit Contracts and Consumer Finance Act (CCCFA).

Can a lender change my loan terms without telling me?

Generally, no. Lenders must provide prior notice of significant changes to loan terms, especially for interest rates or fees, and such changes must be permitted by specific clauses in your original contract. Unilateral changes without notice or contractual basis could be a breach of your rights.

What is considered a ‘predatory loan’ in New Zealand?

While there isn’t a specific legal definition of ‘predatory loan’ in NZ, practices that exploit vulnerable borrowers, such as charging excessively high interest rates or fees, lending irresponsibly without checking affordability, or using aggressive collection tactics, fall under the scope of ‘oppressive’ conduct under the CCCFA and are illegal.

How long do I have to cancel a loan in NZ?

For most consumer credit contracts, you have a 5 working day cooling-off period from when you receive the disclosure statement or sign the contract (whichever is later) to cancel the loan without penalty, beyond repaying the principal and reasonable costs for the period it was active.

Where can I get free advice on my loan contract rights in NZ?

You can seek free, independent advice from organisations like MoneyTalks (a financial capability helpline), the Citizens Advice Bureau, or directly contact a financial dispute resolution scheme like FSCL or the Banking Ombudsman Scheme.

References & Sources