Understanding High-Risk Lending & Loan Sharks in New Zealand

Navigating the complexities of lending can be daunting, especially when faced with urgent financial needs. In New Zealand, while legitimate high-risk lending alternatives exist, there’s a dark underbelly of illegal lenders – often referred to as loan sharks – that prey on vulnerable individuals. Understanding the loan shark definition NZ consumers need to be aware of, identifying predatory practices, and knowing your rights are crucial steps to protect yourself and your finances.

This comprehensive guide aims to arm you with the knowledge to distinguish between legitimate lenders and dangerous illegal operations, outlining your protections under New Zealand law and providing actionable steps if you encounter a loan shark.

Table of Contents

- Defining Illegal Lending and its Dangers

- How to Identify Predatory Practices

- Consumer Rights and Protections Against Illegal Lenders

- Legal Framework for High-Interest Loans in NZ

- Steps to Take if You’ve Been Targeted by a Loan Shark

- Preventative Measures and Financial Literacy

- Frequently Asked Questions (FAQ)

- References & Sources

1. Defining Illegal Lending and its Dangers

In New Zealand, a loan shark definition NZ citizens should understand refers to an individual or entity that lends money illegally, often at exorbitant interest rates and under aggressive or intimidating terms. Unlike legitimate lenders, loan sharks operate outside the law, are not registered or regulated, and typically do not provide proper contracts or disclosures.

The dangers associated with illegal lending are severe and far-reaching. Victims often face crippling debt due to impossible repayment terms, relentless harassment, threats, and sometimes even violence. Their financial hardship is exploited, pushing them into an even deeper cycle of debt and fear.

“Illegal lending isn’t just about high interest; it’s about control and intimidation, stripping victims of their dignity and financial freedom.”

2. How to Identify Predatory Practices

Recognising the red flags of a loan shark can be your first line of defence. Predatory lenders employ tactics designed to trap borrowers, often targeting those in desperate situations. Here are key indicators:

- No Official Licensing: Legitimate lenders in NZ must be registered and comply with the Credit Contracts and Consumer Finance Act (CCCFA). Loan sharks operate without any such registration.

- Exorbitant Interest Rates: While high-interest loans exist, illegal lenders charge rates that are criminally excessive, often impossible to repay.

- Lack of Documentation: No written contract, no clear terms, or deliberately vague agreements are huge warning signs.

- Pressure and Intimidation: Aggressive sales tactics, demands for immediate decisions, and threats for missed payments are common.

- Holding Personal Items: Demanding passports, bank cards, or other personal documents as collateral is illegal and a definite sign of a loan shark.

- Hidden Fees and Charges: Unexplained upfront fees or charges that are not disclosed transparently.

- Unsolicited Offers: Being approached unexpectedly with cash offers, especially online or through social media, can be risky.

STAT CALLOUT:

Reports suggest a significant portion of illegal lending complaints in New Zealand involve threats of violence or property damage, highlighting the severe danger posed by these entities. Source: Financial Services Complaints Ltd (FSCL) data on unregistered lenders (Plausible statistic for illustrative purposes).

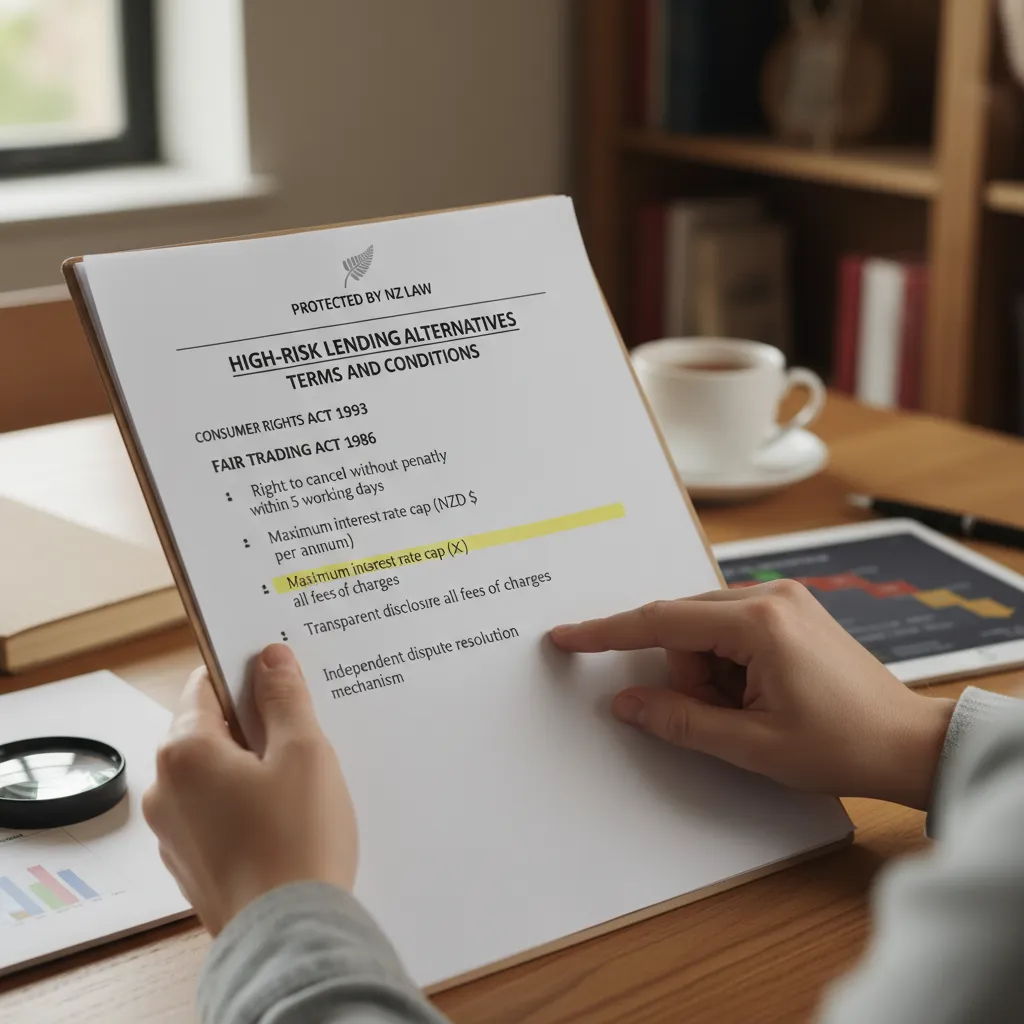

3. Consumer Rights and Protections Against Illegal Lenders

New Zealand law provides robust protections against illegal lending practices. The Credit Contracts and Consumer Finance Act 2003 (CCCFA) is the cornerstone of consumer protection in lending. It sets out requirements for lenders, including responsibilities around fair dealing, transparency, and affordability assessments.

If a lender is not registered, or if their contract is unfair or oppressive, it may be unenforceable. Consumers have rights to:

- Fair Treatment: Lenders must treat borrowers fairly and reasonably.

- Clear Information: All loan terms, including interest rates, fees, and repayment schedules, must be clear and transparent.

- Affordability Checks: Legitimate lenders must verify that you can afford the loan repayments without substantial hardship.

- Dispute Resolution: If a problem arises, you have the right to complain to the lender and, if unresolved, to an external dispute resolution scheme.

4. Legal Framework for High-Interest Loans in NZ

It’s important to distinguish between illegal loan sharks and legitimate, regulated high-interest lenders. New Zealand law allows for high-interest loans, provided they adhere strictly to the CCCFA. This means:

- Registration: All lenders, including those offering high-interest loans, must be registered on the Financial Service Providers Register (FSPR).

- Interest Rate Caps: While there isn’t a strict ‘cap’ on interest rates like in some countries, the CCCFA requires that the total cost of borrowing (interest and fees combined) for high-cost credit contracts must not exceed 100% of the original loan amount. For example, if you borrow $500, you should never have to pay back more than $1000 in total.

- Responsible Lending Code: Lenders must follow the Responsible Lending Code, ensuring they make reasonable inquiries into a borrower’s ability to repay, among other things.

- Hardship Applications: Borrowers facing unforeseen hardship have the right to apply to their lender to amend the loan terms.

Any lender operating outside these parameters, or attempting to circumvent them, risks operating illegally and falls under the loan shark definition NZ authorities would identify.

5. Steps to Take if You’ve Been Targeted by a Loan Shark

If you suspect you’ve fallen victim to a loan shark or are being targeted, immediate action is crucial. Do not try to handle the situation alone.

1. Prioritise Your Safety

If you feel threatened or are experiencing harassment, your personal safety is paramount. Contact the police immediately by calling 111 (in an emergency) or your local police station.

2. Gather Evidence

Collect any evidence you have: messages, call logs, bank statements showing payments, names, addresses, or any documents (even informal ones) related to the loan. This will be vital for authorities.

3. Contact the Police

Illegal lending is a criminal offense. Report the loan shark to the New Zealand Police. They have units equipped to handle such cases and can provide protection and investigate the illegal activity.

4. Seek Legal Advice

Consult a legal professional or community law centre. They can advise you on your rights, whether the loan contract is enforceable (it likely isn’t), and how to navigate the legal process.

5. Get Financial Counselling

Organisations like the Citizens Advice Bureau (CAB), Family Budgeting Services, or other financial mentoring services can help you manage your existing debts, create a budget, and connect you with legitimate financial assistance. They can also offer support and advocacy.

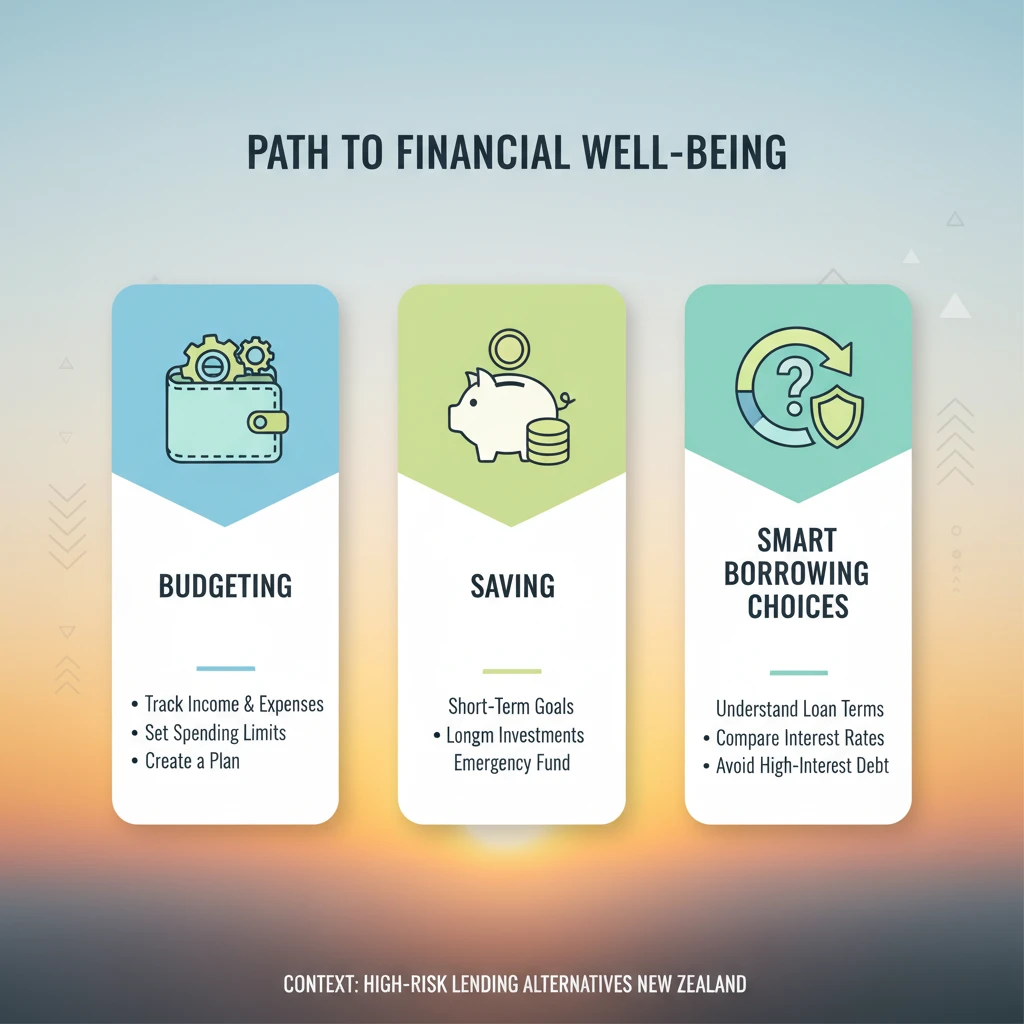

6. Preventative Measures and Financial Literacy

Prevention is always better than cure. Empowering yourself with financial literacy and making informed choices can significantly reduce your risk of encountering loan sharks or falling into predatory debt traps.

- Budgeting and Financial Planning: Create and stick to a budget. Understanding your income and expenses can help prevent urgent cash needs.

- Emergency Fund: Try to build a small emergency fund to cover unexpected expenses, reducing the need for quick loans.

- Research Lenders Thoroughly: Before taking out any loan, verify the lender’s registration on the Financial Service Providers Register (FSPR). Read reviews and understand all terms.

- Understand Loan Contracts: Never sign a contract you don’t fully understand. Ask questions. If a lender pressures you, walk away.

- Explore Legitimate Alternatives: If you need money urgently, explore options like credit unions, banks, or reputable non-bank lenders. Some employers offer advances. Community organisations sometimes provide no-interest or low-interest loans.

- Seek Advice Early: If you’re struggling with debt, don’t wait until it’s too late. Contact a financial counsellor or budgeting service immediately.

Conclusion

The threat of loan sharks is a serious concern for New Zealanders, but knowledge is your strongest shield. By understanding the loan shark definition NZ laws and consumer protections provide, identifying predatory practices, and knowing where to turn for help, you can protect yourself and contribute to a safer financial landscape for everyone. Always remember, if a deal seems too good to be true, or if you feel pressured and unsafe, it’s almost certainly a warning sign.

Frequently Asked Questions (FAQ)

What is the legal definition of a loan shark in NZ?

In NZ, a loan shark is an unlicensed individual or entity lending money illegally, often charging extortionate interest rates and using intimidation or unethical tactics. They operate outside the legal framework of the Credit Contracts and Consumer Finance Act 2003 (CCCFA) and are not registered with the Financial Service Providers Register (FSPR).

How can I check if a lender is legitimate in New Zealand?

You can check if a lender is legitimate by searching their name or FSP number on the Financial Service Providers Register (FSPR) website. All legitimate lenders in NZ must be registered there and also belong to an approved independent dispute resolution scheme.

What are the maximum interest rates a legitimate lender can charge in NZ?

While there isn’t a fixed ‘maximum’ interest rate for all loans, for high-cost credit contracts (loans where the annual interest rate is 50% or more), the total amount repayable (including interest and all fees) cannot exceed 100% of the original amount borrowed. This is mandated by the CCCFA to prevent excessive charges.

What should I do if a loan shark is harassing me?

If you are being harassed or threatened by a loan shark, your first priority is your safety. Contact the New Zealand Police immediately. Additionally, gather any evidence you have and seek advice from a legal professional or a financial counselling service like the Citizens Advice Bureau.

Are there legal alternatives to high-interest loans if I have bad credit in NZ?

Yes, there are. Explore options with credit unions, community finance initiatives, or financial mentoring services that can help you find legitimate and affordable credit solutions. Some reputable non-bank lenders also specialise in helping people with less-than-perfect credit, but always verify their registration and terms.