Understanding APR & Interest Rates on High-Risk Loans

Demystifying the true cost of borrowing in New Zealand’s high-risk lending landscape.

Navigating the world of loans, especially those labelled ‘high-risk,’ can feel like deciphering a complex financial code. For many New Zealanders, understanding the core concepts of APR (Annual Percentage Rate) and how interest rates are calculated is crucial to making informed decisions and avoiding unexpected financial burdens. This comprehensive guide aims to shed light on high interest rates explained NZ, ensuring you understand the true cost of borrowing.

Whether you’re exploring lending alternatives or trying to grasp the nuances of your current commitments, knowing how interest, fees, and charges coalesce into the overall cost is paramount. We’ll break down these critical elements in an authoritative yet approachable manner, empowering you to make smarter financial choices.

What is APR (Annual Percentage Rate)?

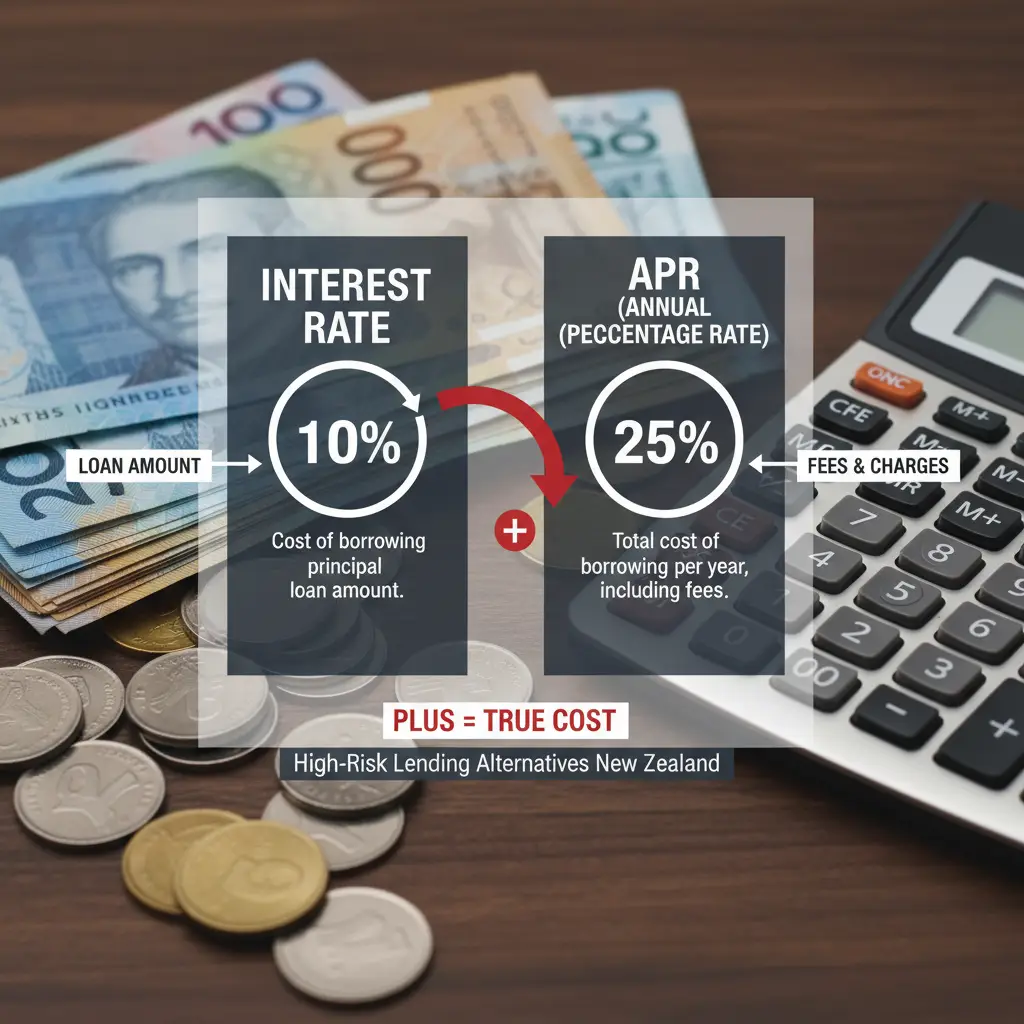

When you see a loan advertised, you’ll often encounter two key terms: ‘interest rate’ and ‘APR’. While often used interchangeably, they represent different aspects of the loan’s cost. The Annual Percentage Rate (APR) is a standardised way to express the true annual cost of borrowing, encompassing not just the nominal interest rate but also most other fees and charges associated with the loan.

In simpler terms, APR gives you a more holistic view of how much you’ll pay over a year for the privilege of borrowing money. It’s designed to make it easier for consumers to compare different loan products, as it includes things like establishment fees, administration fees, and sometimes even compulsory insurance, provided they are factored into the total cost of credit.

“APR is the single most important number to compare when evaluating different loan offers, especially in the high-risk lending sector where fees can significantly inflate the total cost.”

Components of Interest Rates and Fees

Understanding what constitutes your loan’s total cost goes beyond the headline interest rate. For high-risk lending in New Zealand, various components contribute to the overall amount you repay. Here’s a breakdown:

- Nominal Interest Rate: This is the percentage charged on the principal amount borrowed, typically expressed on an annual basis. It’s the core cost of borrowing the money itself.

- Establishment/Application Fees: A one-off charge to cover the lender’s costs of processing your loan application and setting up the account.

- Administration/Service Fees: Regular charges (e.g., weekly, fortnightly, monthly) for maintaining your loan account. These can add up significantly over the loan term.

- Default Fees/Penalty Interest: Charges incurred if you miss a payment or breach the loan agreement. These can be substantial and compound quickly, pushing high interest rates explained NZ even higher.

- Optional Charges: Sometimes, lenders offer ‘optional’ services like payment protection insurance. While not mandatory, they can be presented in a way that makes them seem essential, adding to your total cost.

- Early Repayment Fees: Some lenders charge a fee if you pay off your loan early, designed to compensate them for lost interest.

The cumulative effect of these fees can drastically alter the actual cost of your loan, making a seemingly low nominal interest rate much more expensive in reality.

How High-Risk Lending Rates are Calculated

Lenders assess risk when determining the interest rate they offer. For individuals perceived as ‘high-risk’ – perhaps due to a limited credit history, past financial difficulties, or irregular income – lenders offset this perceived higher risk of default by charging higher interest rates and fees. This is fundamental to understanding high interest rates explained NZ.

Key Factors Influencing High-Risk Loan Rates:

- Credit Score/History: A lower credit score or a history of missed payments signals higher risk.

- Income Stability: Irregular or unverified income can lead to higher rates.

- Debt-to-Income Ratio: A high existing debt load compared to income increases perceived risk.

- Loan Term & Amount: Shorter-term, smaller loans can sometimes carry disproportionately higher APRs due to fixed establishment fees becoming a larger percentage of the principal.

- Collateral: Unsecured loans (without collateral) generally have higher rates than secured loans.

- Market Conditions & Lender’s Cost of Funds: Broader economic factors and the lender’s own borrowing costs also play a role.

High-risk lenders often operate with higher overheads for risk assessment and collections, which further contributes to the elevated rates passed on to borrowers.

The True Cost of Borrowing at High Interest

Understanding the true cost is critical. A high nominal interest rate, coupled with various fees, can lead to a significant repayment burden. This is where the power of APR truly comes into play, as it helps you see the complete picture.

A $2,000 loan repaid over 12 months at a nominal interest rate of 30% might have an APR exceeding 100% when all fees (e.g., $200 establishment fee, $10 weekly administration fee) are included. This means you could repay over double the principal amount.

The cumulative effect can trap borrowers in a cycle of debt. For example, if you borrow $1,000 at a high APR and struggle to make repayments, default fees and penalty interest can rapidly inflate the outstanding balance, making it even harder to escape. This is a common pitfall when navigating high interest rates explained NZ without full comprehension.

It’s not uncommon for the total amount repaid on a high-risk loan to be two, three, or even four times the original principal, especially for smaller, short-term loans with high fixed fees.

Tools for Comparing Effective Interest Rates

To avoid falling into a high-cost trap, actively compare loan offers. Don’t just look at the advertised interest rate; demand to see the full APR and a breakdown of all associated fees. Here’s an action checklist for effective comparison:

Action Checklist: Comparing High-Risk Loan Offers

- Always Request the APR: This is your single best tool for comparing the overall cost of different loans.

- Get a Full Fee Breakdown: Ask for a written list of all establishment, administration, default, and early repayment fees.

- Use Online Calculators: Many financial websites offer loan calculators where you can input the principal, interest rate, and fees to estimate total repayments.

- Compare Total Repayable Amount: Ask each lender for the total amount you will repay over the full term, including all interest and fees.

- Read the Fine Print: Pay close attention to terms and conditions, especially those related to late payments and defaults. Understand how high interest rates explained NZ are structured within the agreement.

- Consider Alternatives: Explore options like credit unions, community finance initiatives, or financial counselling before committing to a high-risk loan.

Empowering yourself with this knowledge means you’re better equipped to navigate the complex landscape of high-risk lending in New Zealand, ensuring you secure a loan that aligns with your financial capacity.

Frequently Asked Questions

What is the difference between APR and interest rate?

The interest rate is the basic cost of borrowing the principal amount, expressed as a percentage. The APR (Annual Percentage Rate) includes the interest rate plus most other fees and charges associated with the loan, providing a more comprehensive measure of its total annual cost. APR is generally the better figure to use for comparing loan offers.

Why are interest rates so high for high-risk loans in NZ?

High-risk lenders charge higher interest rates and fees to compensate for the increased likelihood that some borrowers may default on their loans. Factors like a poor credit history, unstable income, or high existing debt contribute to a borrower being classified as ‘high-risk,’ leading to elevated costs.

How can I reduce the cost of a high-interest loan?

To reduce costs, focus on improving your credit score, ensuring stable income, and minimising other debts before applying. Once you have a loan, make payments on time, consider early repayment if feasible (check for fees), and actively compare offers from different lenders using the APR as your primary comparison tool.

What should I look for when comparing high-interest loan providers in NZ?

Look beyond the nominal interest rate. Prioritise comparing the APR, ask for a full breakdown of all fees (establishment, administration, default), check for early repayment penalties, and calculate the total repayable amount over the loan term. Always read the terms and conditions carefully.

Are there alternatives to high-risk loans in New Zealand?

Yes, explore options such as financial support from family/friends, applying for hardship assistance from existing creditors, seeking no-interest loans (NILs) or low-interest loans from community finance providers, or consulting with a financial counsellor. These alternatives can offer more sustainable solutions.

References & Sources

- Commerce Commission New Zealand. (n.d.). Consumer Credit Law – Responsible Lending. Retrieved from comcom.govt.nz

- Sorted.org.nz. (n.d.). Loans and debt. Retrieved from sorted.org.nz

- Financial Services Complaints Ltd (FSCL). (n.d.). Understanding Loan Contracts. Retrieved from fscl.org.nz

- Ministry of Business, Innovation and Employment (MBIE). (n.d.). Responsible lending obligations for creditors. Retrieved from mbie.govt.nz