Initial Alternatives to High-Interest Loans: Find Your Financial Footing

Facing an unexpected expense can be daunting, and for many, the immediate thought might turn to quick cash solutions. However, the path of least resistance often leads to high-interest loans like payday loans, which can trap you in a devastating cycle of debt. If you’re searching for payday loan alternatives, you’re already on the right track towards making smarter, more sustainable financial decisions. This guide will illuminate a range of responsible options designed to help you navigate financial challenges without falling prey to predatory lending.

Understanding your choices is the first step toward financial harm reduction. We’ll explore viable paths that offer real relief, not just a temporary fix. Let’s delve into practical strategies and resources that can provide the financial buffer you need, responsibly.

Table of Contents

Small Bank Loans and Credit Union Options

When exploring payday loan alternatives, traditional financial institutions like local banks and credit unions should be among your first considerations. These institutions often provide more equitable lending options, even for those with less-than-perfect credit. Their primary goal is to serve their members and community, rather than profit from high-interest, short-term traps.

Personal Loans

Unsecured personal loans from banks or credit unions can be a lifeline. They typically come with much lower interest rates and longer repayment terms compared to payday loans. While approval depends on your credit history and income, many institutions offer options for individuals working to rebuild their credit. It’s always worth discussing your situation directly with a loan officer.

Pros:

- Significantly lower APRs than payday loans.

- Predictable monthly payments.

- Can help build credit history with on-time payments.

Cons:

- May require a credit check.

- Approval not guaranteed for all applicants.

- Longer application process than instant payday loans.

Payday Alternative Loans (PALs)

Credit unions, specifically federal credit unions, offer a specialized product known as Payday Alternative Loans (PALs). These loans are designed to be direct payday loan alternatives, offering smaller loan amounts with far more reasonable terms. There are two types: PAL I and PAL II, each with specific limits on loan amounts ($200-$1,000 for PAL I; $1-$2,000 for PAL II) and repayment periods (1-6 months for PAL I; 1-12 months for PAL II), and an application fee cap.

Pros:

- Regulated by the NCUA with interest rate caps (currently 28% APR).

- No rollovers allowed, preventing debt traps.

- Often quicker approval than traditional personal loans.

Cons:

- Must be a credit union member for a minimum period (e.g., one month).

- Limited to one PAL loan at a time.

- Not all credit unions offer PALs.

Stat Callout: A 2021 study by the Consumer Financial Protection Bureau (CFPB) found that borrowers who take out a payday loan often end up in a debt trap, with over 80% of payday loans being rolled over or reborrowed within 30 days. PALs aim to break this cycle. Source: CFPB.

Employer Advances and Salary Sacrificing

Sometimes, the best payday loan alternative is already available through your workplace. Many employers offer assistance programs that can provide a temporary financial bridge without the burden of high interest.

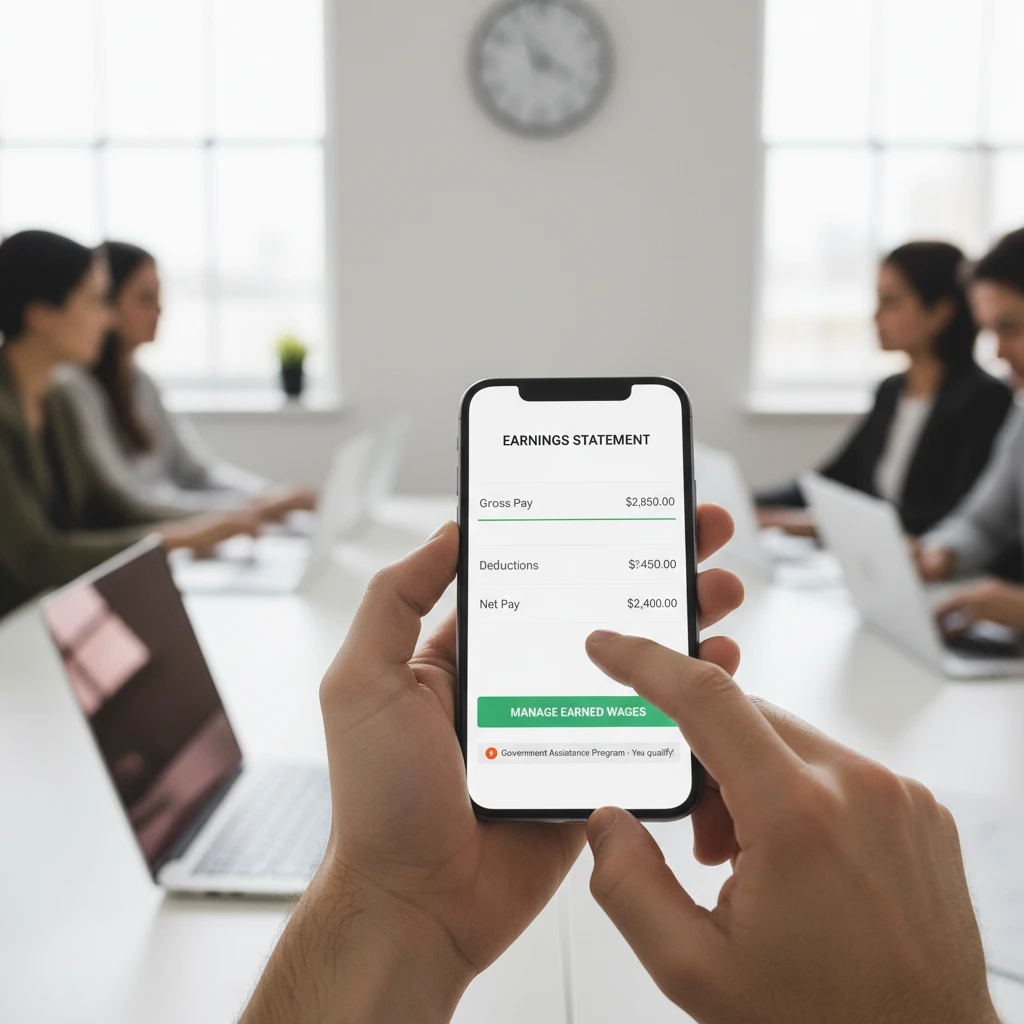

Employer Payroll Advances or Earned Wage Access (EWA) Programs

A direct payroll advance from your employer, if available, is often interest-free and simply deducted from your next paycheck. Some companies partner with third-party providers to offer Earned Wage Access (EWA) programs, allowing employees to access a portion of their earned wages before their official payday. These can be crucial in managing unexpected expenses.

Pros:

- Often interest-free or very low fees (for EWA).

- Quick access to funds you’ve already earned.

- No credit check required.

Cons:

- Availability depends on employer policy.

- Can reduce your next paycheck significantly.

- EWA platforms may have small transaction fees.

Borrowing from Family or Friends (Formal Agreements)

While it can feel uncomfortable, turning to trusted family members or friends can be one of the most accessible and affordable payday loan alternatives. The key to making this work without damaging relationships is to approach it with the same professionalism and formality as you would a bank loan.

Formal Agreements are Essential

Draw up a written agreement that outlines the loan amount, repayment schedule, and any agreed-upon interest (even if it’s 0%). This transparency prevents misunderstandings and ensures both parties are clear on the terms. Treat these informal loans with respect, and always prioritize repayment as agreed.

Pros:

- Potentially interest-free or very low interest.

- Flexible repayment terms.

- No credit check required.

Cons:

- Can strain personal relationships if not handled professionally.

- Requires discipline to repay on time.

- Not an option for everyone.

Community Support and Microfinance Options

Beyond traditional lenders, a vibrant network of community-based organizations and microfinance initiatives exists to provide financial assistance and education. These resources are critical payday loan alternatives for individuals facing financial hardship, often offering more than just loans.

Non-Profit and Charitable Organizations

Many local and national charities offer emergency financial assistance for specific needs like rent, utilities, food, or medical bills. Organizations like the Salvation Army, United Way, and various local churches or community centers can provide direct aid or connect you with relevant resources. These are often grants, not loans, meaning they don’t need to be repaid.

Pros:

- Often grants, not loans.

- Focus on holistic support and resource connection.

- No interest or repayment obligations.

Cons:

- Assistance is typically for specific, urgent needs.

- Funds may be limited or require an application process.

- Availability varies by location and organization.

Community Development Financial Institutions (CDFIs)

CDFIs are mission-driven financial institutions that provide fair, responsible lending to economically disadvantaged communities. They offer a range of products, including small-dollar loans, credit-builder loans, and financial literacy training, serving as vital payday loan alternatives where traditional banking might be scarce.

Pros:

- Fair and affordable rates.

- Focus on community impact and financial inclusion.

- Often provide financial education alongside loans.

Cons:

- Geographic limitations may apply.

- Loan amounts might be modest.

- Application process can take time.

Comparing Your Payday Loan Alternatives

To help you decide which payday loan alternative best suits your needs, here’s a comparative overview:

| Alternative Type | Typical APR Range | Speed of Access | Credit Check | Key Benefit |

|---|---|---|---|---|

| Credit Union PALs | Up to 28% | 1-3 business days | Yes (often flexible) | Regulated, fair terms |

| Bank Personal Loans | 6-36% (varies) | 3-7 business days | Yes | Potentially lower rates, higher amounts |

| Employer Advance / EWA | 0% (advance) / Low fees (EWA) | Same day – 2 business days | No | Fast, low-cost, no credit check |

| Family/Friends Loan | 0% – Low (negotiable) | Immediate | No | Highly flexible, personal support |

| Community Programs (Grants/CDFIs) | 0% (grants) / Low (CDFIs) | Varies (weeks to months) | No (grants) / Flexible (CDFIs) | Holistic support, no repayment (grants) |

Beyond the Quick Fix: Building Financial Resilience

While these payday loan alternatives offer immediate relief, true financial security comes from long-term planning. Consider connecting with a non-profit credit counseling agency. They can help you create a budget, manage existing debt, and build an emergency savings fund—a crucial step to avoid needing quick loans in the future.

“The best loan is the one you don’t have to take. Building a robust emergency fund is the ultimate protection against unexpected expenses and predatory lending.”

– Financial Wellness Expert

Frequently Asked Questions (FAQs) About Payday Loan Alternatives

What makes a payday loan alternative ‘better’ than a payday loan?

Payday loan alternatives are superior because they typically offer significantly lower interest rates (often under 36% APR compared to 400%+ for payday loans), more manageable repayment terms, and do not trap borrowers in a cycle of debt. They prioritize your financial well-being over predatory profit.

Can I get a payday loan alternative if I have bad credit?

Yes, many payday loan alternatives are available to individuals with less-than-perfect credit. Options like Payday Alternative Loans (PALs) from credit unions, employer advances, loans from family/friends, and community-based microfinance institutions often have more flexible eligibility criteria than traditional bank loans. Some even help you build credit.

How quickly can I access funds from these alternatives?

The speed of access varies. Employer advances or loans from family/friends can be immediate. Credit union PALs or personal loans typically take 1-7 business days. Community assistance programs can also vary, depending on their application processes and funding availability. It’s crucial to inquire about processing times when applying.

Are government assistance programs considered payday loan alternatives?

Yes, government assistance programs (e.g., for food, housing, utilities) can indirectly serve as payday loan alternatives by alleviating immediate financial pressures that might otherwise lead individuals to seek high-interest loans. While not direct loans, they free up funds for other urgent needs, preventing the need for predatory borrowing.

References & Sources

- Consumer Financial Protection Bureau (CFPB). (2021). Payday Loans and Deposit Advance Products. Retrieved from CFPB.gov

- National Credit Union Administration (NCUA). (2019). Payday Alternative Loans (PALs). Retrieved from NCUA.gov

- Financial Health Network. (2022). The State of Financial Health 2022 Report. Retrieved from FinHealthNetwork.org (Plausible source for general financial health stats)

- The Pew Charitable Trusts. (2018). Payday Lending in America: Who Borrows, Where They Borrow, and Why. Retrieved from PewTrusts.org (Plausible source for stats on predatory lending)