Buy Now Pay Later NZ risks primarily involve the accumulation of unmanageable debt through multiple platforms, leading to financial strain and damaged credit scores. Without the rigorous affordability checks of traditional lending, consumers may overcommit, resulting in late fees and negative impacts on future mortgage approvals or rental applications due to perceived poor cash flow management.

The Modern Debt Spiral: Is BNPL the New Payday Loan?

In the evolving landscape of New Zealand’s financial sector, Buy Now Pay Later (BNPL) services have rapidly shifted from a niche payment option to a ubiquitous method of transaction. While marketed as a budgeting tool and a convenient alternative to credit cards, financial experts are increasingly categorizing BNPL as a modern iteration of the payday loan—albeit with a slicker interface and better branding. The core mechanism remains dangerously similar: obtaining goods immediately while deferring payment against future income.

The psychological allure of BNPL lies in the separation of the ‘pain of paying’ from the ‘pleasure of purchasing.’ When a consumer spends $200 on clothing but only sees an upfront cost of $50, the immediate financial friction is reduced by 75%. This phenomenon, known as payment decoupling, encourages consumers to spend more than they would if they were using cash or a debit card. Unlike traditional layby where the extensive wait time allowed for a ‘cooling off’ period, BNPL provides instant gratification with deferred consequences.

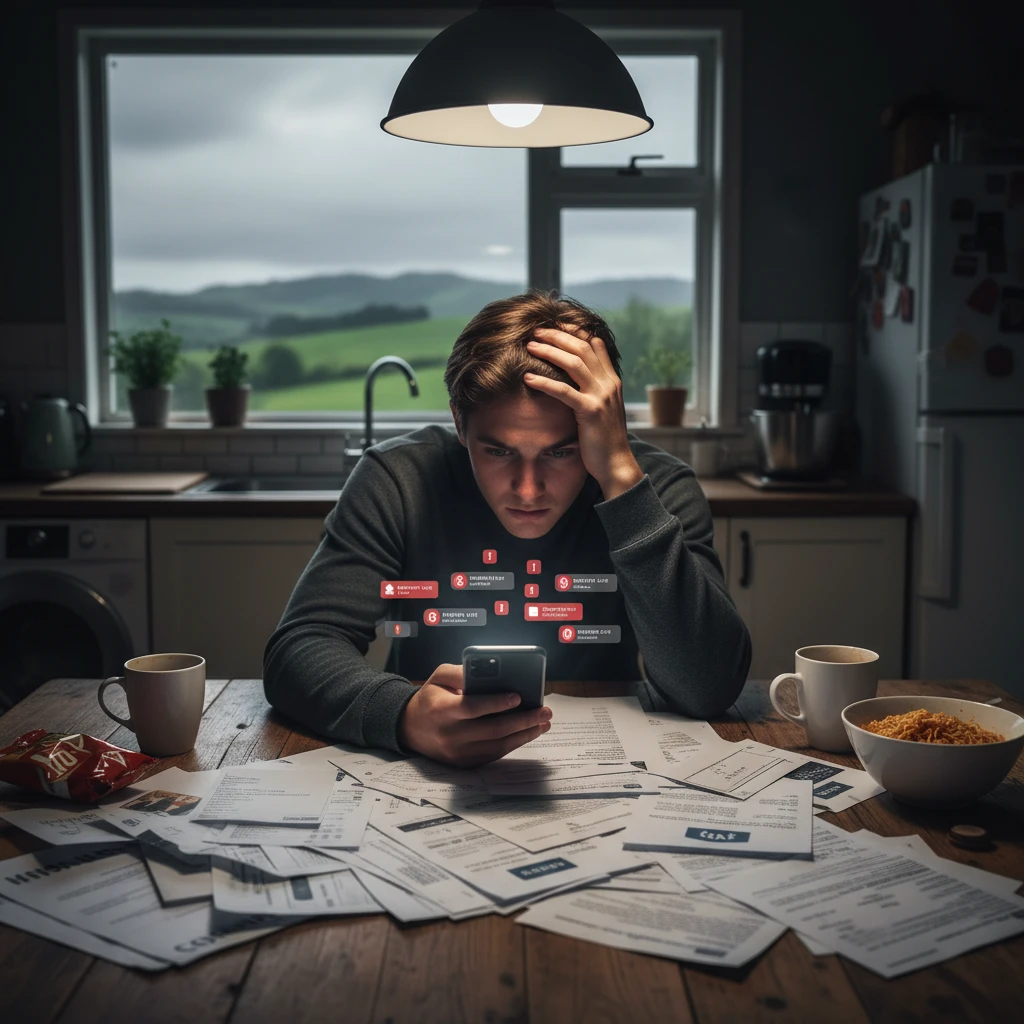

For many Kiwi households, BNPL is no longer used solely for discretionary luxury items. Data suggests an increasing trend of users relying on these services for essentials, such as groceries and utilities, often purchasing gift cards via BNPL platforms to pay for basic living costs. This behavior signals a dependency cycle similar to the debt spirals seen with high-interest payday lenders. When next week’s pay is already earmarked for four or five different repayment schedules, the borrower is left with a cash deficit, prompting further borrowing to survive the week. This cyclical trap is the definition of a debt spiral, and it is happening without the consumer ever stepping foot in a lending office.

The Regulatory Gap: BNPL vs. Traditional Credit

One of the most significant risks associated with the BNPL sector in New Zealand has been the historical lack of regulation compared to traditional credit providers. Until recently, BNPL providers fell into a regulatory grey area. Because they do not technically charge “interest” (instead charging late fees), they were not subjected to the full weight of the Credit Contracts and Consumer Finance Act (CCCFA) in the same way banks and personal loan providers were.

When you apply for a credit card or a personal loan from a New Zealand bank, the lender is legally obligated to conduct a forensic analysis of your finances. They must verify your income, scrutinize your expenses, and stress-test your ability to repay the debt without suffering substantial hardship. This process, while sometimes cumbersome, acts as a critical safety barrier against predatory lending and over-indebtedness.

In contrast, BNPL providers have historically utilized ‘soft’ credit checks or no credit checks at all for smaller amounts. The algorithm approves spending limits based on the user’s repayment history with that specific platform, rather than their holistic financial position. This means a user could have maxed-out limits on Afterpay, Zip, and Laybuy simultaneously, and a new provider would have no visibility of this existing debt burden. While the government is moving to bring BNPL closer to CCCFA regulations to ensure affordability checks are implemented, the legacy of this ‘wild west’ environment has left many Kiwis with debt-to-income ratios that traditional lenders would deem high-risk.

The absence of centralized reporting for all BNPL transactions means that the total debt exposure of a consumer is often invisible until it becomes a crisis. This regulatory gap places the onus of responsible lending entirely on the consumer’s self-control, which, given the sophisticated behavioral psychology employed by these apps, is a significant mismatch in power.

The Trap of Stacking: Managing Afterpay, Laybuy, and Zip

The term “stacking” refers to the practice of holding active accounts with multiple BNPL providers simultaneously. In New Zealand, the market is saturated with options including Afterpay, Laybuy, Zip, Klarna, and Humm. While a single repayment of $25 a week is manageable for most income earners, the danger arises when a consumer stacks multiple repayments across different platforms.

Consider a scenario where a consumer has three active orders on Afterpay ($75/week), two on Zip ($50/week), and a rolling subscription on Laybuy ($30/week). Individually, these purchases seemed affordable at the checkout. Collectively, they represent a weekly outflow of $155. For a student, a part-time worker, or a family on a tight budget, this uncommitted monthly income drain can be catastrophic.

The Impact of Late Fees

The revenue model for many BNPL schemes relies heavily on merchant fees, but late fees from consumers are a substantial component. The risk of stacking is that it increases the logistical complexity of money management. Tracking due dates across three or four different apps increases the probability of human error. A missed payment on a traditional credit card might incur a single fee and interest. Missed payments across four BNPL orders can trigger four separate late fees instantly.

Furthermore, the “gamification” of these platforms often masks the total liability. Users are encouraged to unlock higher spending tiers by making payments on time. This creates a perverse incentive to spend more to “level up” their account status, effectively rewarding the accumulation of debt. This is distinct from a credit card limit increase, which is usually tied to income verification; BNPL limit increases are often tied merely to the velocity of spending and repayment.

The Real Cost: Impact on Mortgage and Rental Applications

Perhaps the most severe, long-term risk of Buy Now Pay Later in NZ is its impact on future financial mobility. There is a common misconception that because BNPL is “interest-free,” it does not count as “real debt” in the eyes of banks. This is factually incorrect and dangerous thinking for anyone aspiring to buy a home.

When assessing a mortgage application, New Zealand banks scrutinize three main areas: income, credit history, and expenses. BNPL impacts the latter two significantly.

1. Reduction of Borrowing Power

Banks view BNPL repayments as a fixed commitment. If you have recurring BNPL payments, a bank will annualize this cost and deduct it from your serviceable income. Even if you pay off your balance in full every few weeks, a pattern of consistent BNPL usage signals to the bank that you have higher living expenses. For every dollar committed to a BNPL repayment, your borrowing power for a mortgage is reduced by a multiple of that amount. A consistent $50 weekly repayment could reduce your potential mortgage lending by upwards of $20,000 to $30,000 depending on the bank’s calculator.

2. Perception of Financial Management

Beyond the math, there is the behavioral assessment. Mortgage brokers and bank assessors look for “clean” account conduct. A bank statement riddled with payments to Afterpay, Laybuy, and liquor stores or fast food outlets paints a picture of a consumer who lives paycheck to paycheck and relies on short-term credit for discretionary spending. This is a red flag for lenders who are looking for stability and the ability to save. Lenders prefer to see a surplus of uncommitted income accumulating in a savings account, not a frantic cycle of micro-repayments.

Rental applications are also affected. In a competitive rental market, property managers often request bank statements or credit checks. A tenant with a history of BNPL late fees or excessive usage may be viewed as a higher risk for rental arrears compared to a tenant with simpler banking habits. The presence of defaults on a credit report from BNPL providers (which does happen if debts are passed to collection agencies like Baycorp) can instantly disqualify a tenant from securing a property.

Financial Safety: How to Break the Cycle

Recognizing the risks is the first step; taking action to mitigate them is the second. If you find yourself caught in the BNPL trap, there are specific strategies to regain control of your financial health.

- The Snowball Method: List all your BNPL buy-outs from smallest to largest. Pay the minimums on all of them, but throw any extra cash at the smallest balance. The psychological win of closing an account entirely provides momentum to tackle the next one.

- Delete the Apps: This sounds simple, but the friction is necessary. Remove the apps from your phone to stop the temptation of “impulse” adding to your debt stack. Unsubscribe from their marketing emails which are designed to trigger FOMO (Fear Of Missing Out).

- Switch to Debit: Re-train your brain to spend only what you currently possess. If the money isn’t in the account, the purchase cannot be made. This reconnects the pain of paying with the purchase, naturally curbing spending.

- Seek Financial Mentoring: In New Zealand, services like MoneyTalks provide free budgeting advice. They can help negotiate with creditors if you are facing genuine hardship and cannot meet your repayment obligations.

Buy Now Pay Later is not inherently evil, but it is a financial product designed to maximize consumption. In the current economic climate of New Zealand, treating it with the same caution as a credit card or a personal loan is essential for maintaining long-term financial safety.

Does Afterpay affect credit score NZ?

Yes, it can. While Afterpay does not always perform a hard credit check upon sign-up, if you miss payments and your debt is sent to a debt collection agency, a default will be listed on your credit file (such as Centrix or Equifax). This default can remain on your record for five years and significantly damage your credit score.

Can I get a mortgage with BNPL debt?

It is more difficult. Banks view BNPL repayments as an expense that reduces your disposable income. Having active BNPL debts reduces the total amount you can borrow. Furthermore, a history of heavy BNPL usage can signal to the bank that you have poor cash flow management, potentially leading to a declined application.

Is Laybuy regulated in NZ?

The regulatory environment is tightening. The New Zealand government has announced regulations to bring BNPL providers under the Credit Contracts and Consumer Finance Act (CCCFA). This means providers like Laybuy will be required to conduct affordability checks to ensure they are not lending to vulnerable consumers who cannot repay.

What happens if I don’t pay Zip NZ?

If you miss payments with Zip NZ, you will be charged late fees. If the debt remains unpaid, your account will be suspended, preventing further purchases. Eventually, the debt may be passed to a third-party collection agency, which will add collection costs to your debt and record a default on your credit file.

Are BNPL schemes truly interest-free?

Technically, most are interest-free if paid on time. However, they monetize through merchant fees and late payment fees. If you miss payments, the accumulated late fees can equate to a high effective interest rate. Some longer-term BNPL products (like those for higher value items) may charge establishment fees or interest.

How do I cancel BNPL accounts permanently?

To cancel accounts like Afterpay, Zip, or Laybuy, you must first pay off all outstanding balances. Once the balance is zero, you can usually close the account via the app’s settings menu or by contacting their customer support. It is recommended to delete the app immediately after closing the account to prevent reactivation.