Back to school loans NZ are short-term personal finance options marketed to parents in New Zealand to cover costs like uniforms, stationery, and digital devices. While they offer immediate cash, these loans often come from third-tier lenders with high interest rates and strict repayment terms. Financial advisors strongly recommend exploring Work and Income (WINZ) recoverable assistance or no-interest community loans before accepting high-cost private debt.

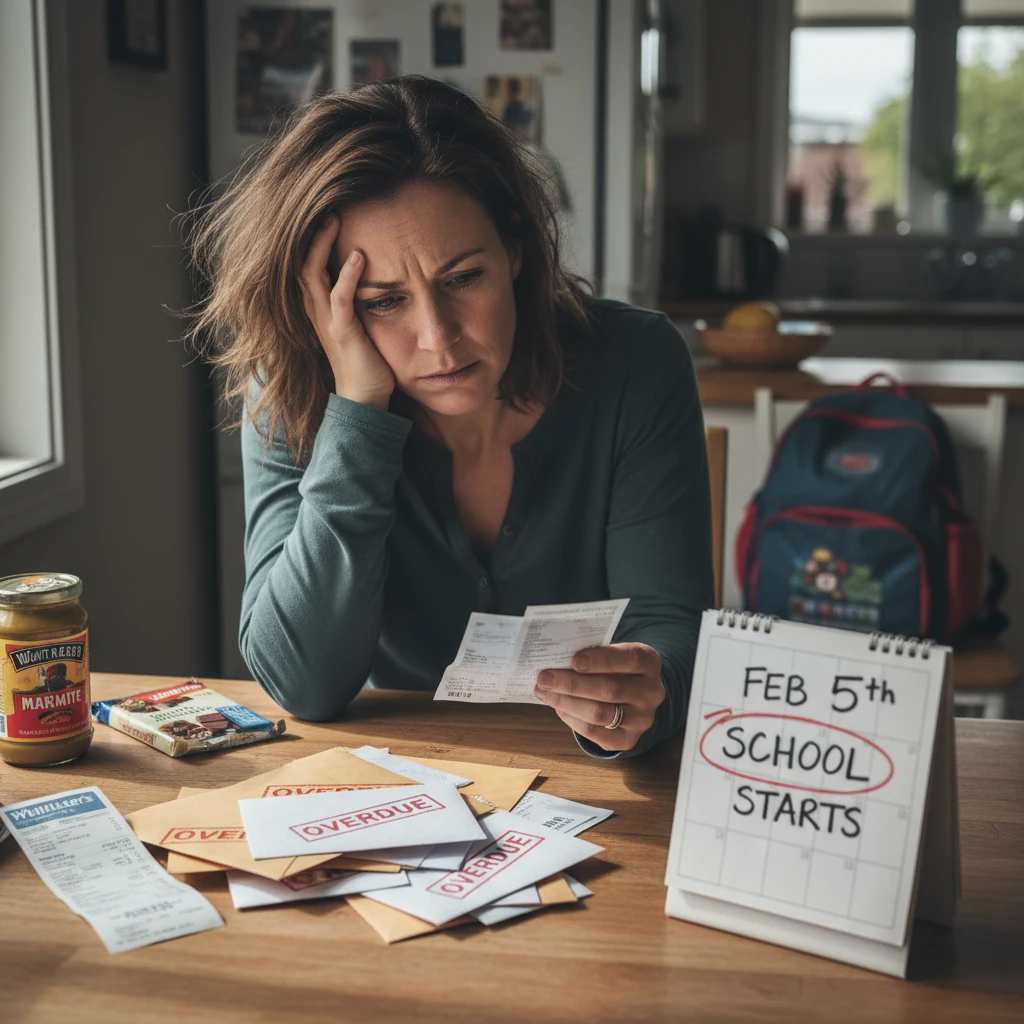

The transition from the festive season into the new academic year creates a perfect storm for financial stress. For many New Zealand whānau, the pressure to provide adequate schooling resources clashes with the financial exhaustion of December. This guide explores the risks of seasonal borrowing, specifically targeting predatory lending practices, and offers safer, sustainable alternatives for managing education costs.

The December Debt Hangover: Managing Christmas Spending

In New Zealand, the cultural expectation to overspend during Christmas often leaves families vulnerable just as the school year begins. This phenomenon, known as the “December Debt Hangover,” is the primary driver for the demand for back to school loans in NZ. When credit cards are maxed out and savings are depleted by late December, the arrival of January bills creates a liquidity crisis.

The psychological pressure to provide a “good Christmas” often overrides long-term financial logic. Retailers aggressively market Buy Now, Pay Later (BNPL) schemes and store cards, encouraging consumers to push payments into the new year. However, when these payments fall due in late January, they coincide exactly with the release of school stationery lists and uniform requirements.

The Compound Interest Effect

The danger lies not just in the spending, but in how it is financed. If Christmas was funded through high-interest credit cards or third-tier lenders, the interest begins to compound immediately. By the time parents are looking for back to school loans, they are often already servicing significant debt. Adding a new loan to cover uniforms effectively means paying interest on interest, trapping families in a cycle that can take the entire year to break.

January Pressure: Uniforms and Device Financing Scams

The cost of a “free” education in New Zealand has risen dramatically, primarily driven by the cost of uniforms and the mandatory requirement for digital devices (BYOD – Bring Your Own Device). This pressure creates a fertile hunting ground for predatory lenders and mobile truck shops.

The BYOD Financing Trap

Most intermediate and secondary schools in New Zealand now require students to have a laptop or Chromebook. While a basic Chromebook might retail for $350 to $450 at a standard electronics store, families with bad credit or no cash flow often turn to alternative financing or mobile traders.

Warning Signs of Predatory Device Financing:

- Inflated Base Prices: A device worth $400 may be listed for $1,200.

- Weekly Payment Illusions: “Only $20 a week” sounds affordable, but over a three-year contract, the total cost becomes astronomical.

- Obsolete Technology: By the time the device is paid off, it is often outdated or broken, yet payments must continue.

Uniform Monopolies and Costs

School uniforms are often sold by a single supplier, eliminating price competition. A full kit for a high school student can easily exceed $500. Predatory lenders know this is a non-negotiable expense for parents who want their children to fit in and avoid disciplinary action. Consequently, they market “fast cash” loans specifically for this purpose, often glossing over establishment fees that can add hundreds of dollars to the principal amount.

Understanding Predatory Back to School Loans

When searching for “back to school loans nz,” users will encounter a mix of legitimate bank offers and highly predatory third-tier lenders. It is crucial to distinguish between the two to ensure financial safety.

What makes a loan predatory?

In the New Zealand context, predatory lending often involves targeting vulnerable communities with terms that are technically legal but ethically dubious. Despite the tightening of the Credit Contracts and Consumer Finance Act (CCCFA), high-cost lenders still operate.

Key characteristics include:

- Interest Rates near 50%: Some lenders charge the maximum allowable interest rates.

- excessive Default Fees: Missing a payment results in penalties that far exceed the administrative cost of the error.

- Direct Debits from Benefits: Lenders often require authority to take payments directly from benefits or wages before the borrower sees the money, leaving families without money for food.

The “Truck Shop” Phenomenon: Mobile traders that drive into low-income neighborhoods selling stationery and uniforms on credit are a specific concern. The Commerce Commission has prosecuted several for failing to disclose total costs, yet they remain a common source of seasonal debt.

Safe Alternatives to High-Interest Debt

Before applying for a private back to school loan, New Zealand parents should exhaust all available government and community support options. These alternatives are designed to prevent hardship rather than profit from it.

Work and Income (WINZ) Recoverable Assistance

If you are on a benefit or have a low income, you may qualify for a Recoverable Assistance Payment or an Advance Payment from Work and Income. This is essentially an interest-free loan.

- Scope: Can cover uniforms, stationery, and school fees.

- Repayment: Repayments are deducted from your benefit or wages at a manageable rate without interest.

- Eligibility: You do not necessarily need to be on a main benefit to qualify, depending on income limits and asset tests.

Good Shepherd NZ: No Interest Loans (NILS)

Good Shepherd NZ, in partnership with BNZ and community providers (like the Salvation Army), offers No Interest Loans (NILS) for essential costs. These loans allow families to borrow up to $1,500 for essentials like educational devices and uniforms with zero interest and no fees. This is the gold standard alternative to predatory back to school loans.

School-Based Payment Plans

Many schools are aware of the financial strain on families. Before taking out a loan, contact the school office. Many schools allow:

- Drip-feeding costs: Paying off uniforms or camps over the course of the year.

- Hardship funds: Some schools have discretionary funds or access to charity grants to subsidize uniforms for families in need.

Winter Energy Payment vs. Heating Loans

The cycle of seasonal debt rarely ends in February. Loans taken out for back-to-school costs often have repayment terms that stretch into the winter months, colliding with rising energy bills. This creates a dangerous dynamic regarding the Winter Energy Payment (WEP).

The Purpose of the Winter Energy Payment

The WEP is a government initiative designed to help seniors and beneficiaries heat their homes from May to October. However, budget advisors report that many families use this payment to service the high-interest debt accumulated during the back-to-school period.

The Risks of Misallocating WEP

Using the Winter Energy Payment to pay off a 49% interest loan might seem like a good financial move to reduce debt, but it often leads to “heating loans” or falling behind on power bills later in the season. Heating loans are another form of predatory finance marketed aggressively in May and June.

Strategy: If you are struggling with back-to-school debt as winter approaches, engage with a financial mentor (MoneyTalks) immediately. They can negotiate with lenders to freeze interest or restructure payments so that your WEP can remain dedicated to keeping your whānau warm and healthy.

Planning Ahead: Breaking the Cycle

Breaking the cycle of seasonal debt requires shifting from reactive borrowing to proactive saving. While this is difficult when money is tight, even small changes can insulate families from the need for high-interest back to school loans in the future.

Christmas Clubs and Supermarket Stamps

Old-fashioned Christmas clubs or supermarket stamp schemes (like Pak’nSave) are effective because they lock funds away until December/January. By accumulating grocery value throughout the year, you free up cash flow in January that would otherwise be spent on food, allowing that cash to be redirected to uniforms and stationery.

Dedicated “Back to School” Accounts

Opening a separate bank account specifically for education costs can be psychologically powerful. Setting up an automatic payment of $5 or $10 a week starting in February ensures that by the following January, you have a buffer of $260-$520. This may not cover everything, but it significantly reduces the amount that needs to be financed, thereby reducing interest costs.

Buying Second Hand

Reduce the principal amount needed by utilizing second-hand uniform shops. Most schools run these, and the quality is often excellent. For devices, consider refurbished corporate laptops from reputable IT recyclers, which are often more robust and cheaper than new consumer-grade Chromebooks sold on credit.

People Also Ask

Can WINZ help with school uniforms in NZ?

Yes, Work and Income (WINZ) can provide assistance for school uniforms and stationery costs. This is usually done through a Recoverable Assistance Payment, which is an interest-free loan that you pay back over time from your benefit or wages. Eligibility depends on your income and asset levels.

What is the school start-up payment?

The School Start-up Payment is a specific assistance available to those caring for someone else’s child (e.g., Unsupported Child’s Benefit or Orphan’s Benefit). It is a non-taxable payment to help with the costs of clothing and other school-related needs at the beginning of the year.

How to pay for school stationery with no money?

If you have no funds, contact Work and Income for an advance. Alternatively, check if your school has a partnership with charities like KidsCan, or inquire about the Good Shepherd No Interest Loan Scheme (NILS). Avoid using high-interest payday lenders.

Are mobile trader trucks legal in NZ?

Yes, mobile trader trucks are legal, but they are strictly regulated under the Credit Contracts and Consumer Finance Act (CCCFA). They must disclose all costs and interest rates upfront. The Commerce Commission actively monitors them for predatory behavior and has prosecuted several for illegal practices.

Does the Winter Energy Payment affect my loan eligibility?

Lenders may view the Winter Energy Payment as income, but responsible lenders should not include it when calculating your ability to service a long-term loan, as it is a temporary seasonal payment intended specifically for energy costs.

What is a NILS loan?

NILS stands for No Interest Loan Scheme. In New Zealand, these are provided by Good Shepherd. They allow qualifying individuals to borrow up to $1,500 for essential goods and services (like education costs) without paying any interest or fees, offering a safe alternative to predatory debt.