Car finance scams in West Auckland typically involve predatory dealers targeting vulnerable buyers with “$1 deposit” offers that mask exorbitant interest rates and hidden fees. These schemes often bundle overpriced Mechanical Breakdown Insurance with poor-quality vehicles, trapping consumers in unmanageable debt cycles that may violate the Credit Contracts and Consumer Finance Act (CCCFA).

The Reality of Vehicle Finance Traps in Auckland

For many residents in West Auckland and surrounding suburbs, securing a vehicle is essential for employment and family logistics. However, the desperation to secure transport often leads consumers into the hands of predatory lenders. While legitimate dealerships operate with transparency, a subset of “second-tier” and “third-tier” lenders aggressively market to those with bad credit, often using deceptive tactics that border on fraud.

These financial traps are not merely bad deals; they are sophisticated systems designed to maximize profit from those who can least afford it. By focusing on weekly payments rather than the total cost of credit, dealers obscure the reality that the borrower may end up paying three to four times the vehicle’s actual value.

The ‘$1 Deposit’ Car Loan Trap Explained

One of the most pervasive marketing tactics seen in West Auckland car yards is the “$1 Deposit” or “No Deposit” sign. While this appears to be an accessible entry point for families struggling with cash flow, it is frequently the primary mechanism of a finance trap.

The Mathematics of the Trap

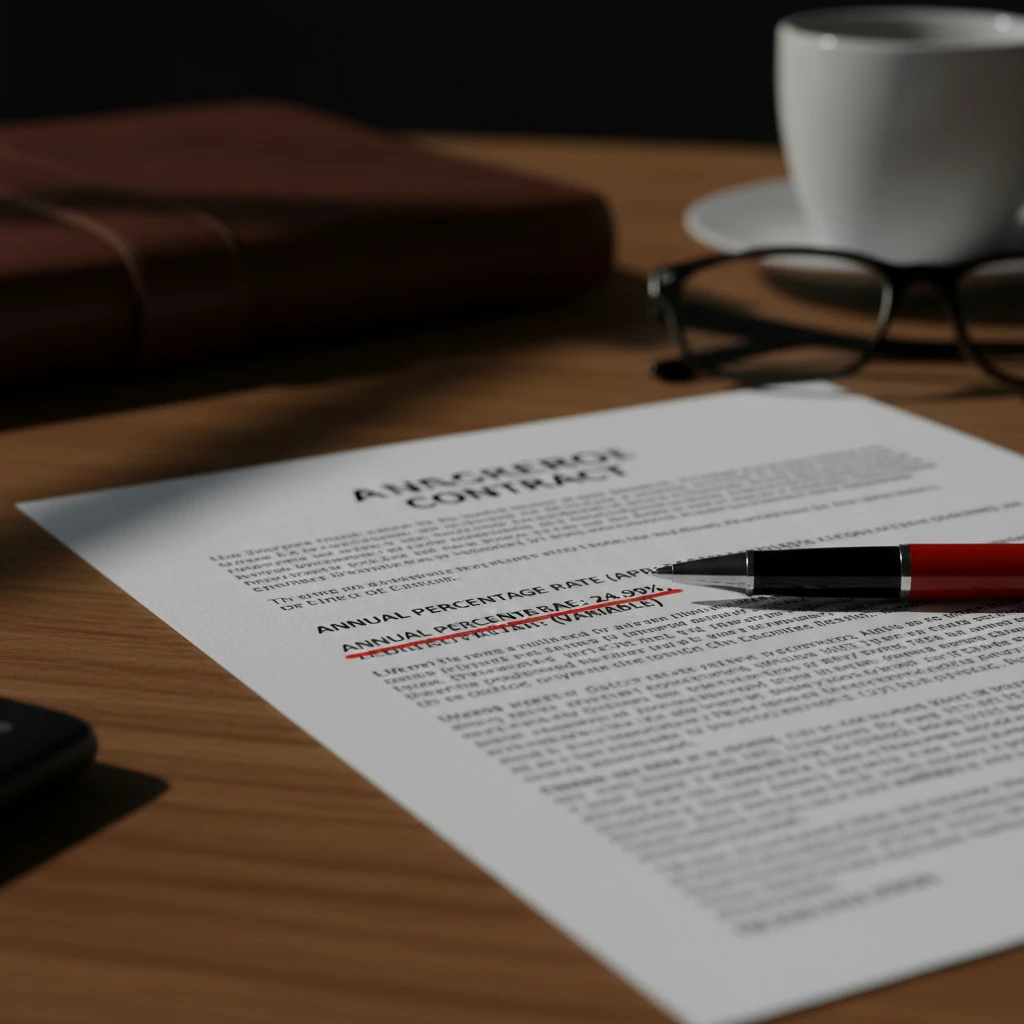

When a dealer accepts a negligible deposit, the risk to the lender increases. To mitigate this risk, they apply significantly higher interest rates—often between 20% and 29.95% per annum. Furthermore, because there is no initial equity in the vehicle, the loan amount is higher, leading to more interest accumulating over the term.

Consider a vehicle with a sticker price of $10,000. With a standard deposit and a fair interest rate (e.g., 9-12%), the total cost of credit might be manageable. However, under a predatory “$1 deposit” scheme with a 28% interest rate over 48 months, the total repayment can easily exceed $18,000. The borrower is immediately in a position of negative equity: they owe far more than the car is worth the moment they drive it off the lot.

The “Weekly Payment” Illusion

Predatory lenders in West Auckland are trained to deflect questions about interest rates or total cost. Instead, they fixate the buyer on the “weekly payment.” By stretching the loan term to 48 or 60 months, they can make an expensive loan appear affordable. A payment of $90 a week sounds manageable, but over five years, it represents a catastrophic financial loss for a low-income household.

How Predatory Dealers Target Beneficiaries

A disturbing trend identified by financial mentors and the Commerce Commission is the specific targeting of beneficiaries and low-income workers. While this issue is prevalent across Auckland, specific corridors in West and South Auckland have high concentrations of dealerships employing these tactics.

Exploiting WINZ Payments

Unethical dealers are well-versed in the Work and Income NZ (WINZ) system. They often market directly to beneficiaries, promising that “WINZ payments are welcome.” The trap here is psychological; by suggesting that the government benefit will cover the loan, they lower the buyer’s guard regarding the total debt load. In some egregious cases, dealers have been known to drive customers to WINZ offices or assist them in filling out incomplete budget forms to ensure the loan is approved, despite the borrower’s inability to afford the necessities of life.

Pressure Sales Tactics

Vulnerable buyers are often subjected to high-pressure environments. This includes keeping the buyer at the yard for hours, using “limited time” offers, or claiming another buyer is interested in the same vehicle. For someone needing a car to get to a new job, this pressure can force a hasty signature on a contract that has not been properly read or understood.

The ‘Lemon’ Car and Loan Bundle

A “lemon” is a vehicle with significant manufacturing defects or mechanical issues that affect its safety, value, or utility. In the context of car finance scams in West Auckland, the “Lemon Bundle” is a particularly devastating trap.

The Double Jeopardy of Debt and Repair

In this scenario, a dealer sells a high-mileage, poor-quality import at an inflated price using high-interest finance. Within months, the car suffers a catastrophic mechanical failure. The borrower is now left with a vehicle that cannot be driven but still has four years of loan payments remaining.

Many borrowers erroneously believe they can stop paying the loan if the car stops working. This is legally incorrect. The finance contract is usually with a third-party finance company, not the dealer. The finance company demands payment regardless of the vehicle’s condition. This leads to credit defaults and repossession.

The Junk Insurance Add-On

To counter the fear of mechanical failure, predatory dealers aggressively upsell Mechanical Breakdown Insurance (MBI) and Payment Protection Insurance (PPI). While insurance is generally good, these specific policies are often “junk products.” They are sold at highly inflated premiums (which are added to the loan, incurring interest) but contain so many exclusions and clauses that they rarely pay out when needed. A policy costing the dealer $300 might be sold to the consumer for $1,500, plus 25% interest over three years.

Your Rights: The CCCFA and Responsible Lending

New Zealand consumers are protected by the Credit Contracts and Consumer Finance Act (CCCFA). Recent amendments to this act have tightened the rules significantly to prevent the exact types of car finance scams West Auckland residents face.

The Lender’s Responsibility

Under the Responsible Lending Code, lenders must:

- Make Reasonable Inquiries: They must verify your income and expenses to ensure you can make payments without suffering substantial hardship. If a lender did not properly check your budget, the loan might be unenforceable.

- Assist Informed Decisions: Lenders must ensure you understand the key terms of the contract. Hiding the interest rate or rushing the signing process is a breach of this duty.

- Treat Borrowers Reasonably: This applies throughout the loan, including if you miss payments.

Right to Cancel

You have a short “cooling-off” period after signing a finance contract. Usually, this is 5 working days if you received the disclosure statement in person. If you realize you have been trapped in a bad deal, you must act immediately to cancel the contract in writing.

Repossession Laws: What Agents Can and Cannot Do

Fear of repossession keeps many victims of predatory lending silent. However, New Zealand law strictly governs how and when a vehicle can be repossessed. Repossession agents cannot act like cowboys; they must follow due process.

The Pre-Possession Process

Before a lender can repossess your car, they must generally be in default (behind on payments) and the lender must have sent a “Repossession Warning Notice.” You must be given at least 15 days to remedy the default (pay the arrears) before they can take the car.

Prohibited Behavior

Repossession agents:

- Cannot enter your home forcibly.

- Cannot enter your property outside the hours of 6 am to 9 pm (Monday to Saturday) or on Sundays and public holidays (unless you gave specific written consent in the contract).

- Must treat you and your property with respect. They cannot use physical violence or intimidation.

Red Flags: How to Identify a Predatory Dealer

To protect yourself from car finance scams in West Auckland, be vigilant for these warning signs:

- No Window Cards: Every car for sale by a dealer must have a Consumer Information Notice (CIN) card in the window. If it’s missing, walk away.

- Blank Documents: Never sign a document that has blank spaces where numbers should be.

- “Today Only” Deals: Legitimate finance offers do not expire in 24 hours. This is a pressure tactic.

- Refusal to Let You Take Papers Home: You have the right to take the contract home to read it or show it to a budget advisor. If they refuse, they are hiding something.

If you suspect you have been targeted by a predatory lender, contact the Commerce Commission or a local budget mentoring service immediately. You may have grounds to have the debt reduced or the contract cancelled.

Can I return a car if I can’t afford the finance in NZ?

Generally, you cannot simply return a car because you can no longer afford it. However, you can conduct a “voluntary return” of the vehicle to the lender. The lender will sell the car to cover the debt. Be aware that if the car sells for less than what you owe, you are still liable for the remaining balance (the shortfall).

What is the maximum interest rate for car loans in NZ?

There is no specific legal cap on interest rates in New Zealand, provided the rate is not “oppressive.” However, under the CCCFA, the total cost of credit must not be oppressive. Rates above 30% are increasingly scrutinized, but many second-tier lenders still charge between 18% and 29.95%.

How do I complain about a car finance company?

First, complain directly to the lender. If they do not resolve the issue, you can escalate the complaint to their dispute resolution scheme (such as the Financial Services Complaints Ltd or the Insurance & Financial Services Ombudsman). All lenders must belong to one of these schemes.

Does the Consumer Guarantees Act cover used cars?

Yes. If you buy a vehicle from a registered motor vehicle trader (dealer), the Consumer Guarantees Act (CGA) applies. The vehicle must be of acceptable quality. This protection does not apply to private sales.

Can a repo agent enter my house?

No. A repossession agent can enter your property (the land/driveway) to take the car if they have the legal right, but they cannot force entry into your dwelling (house) to get keys or the vehicle without a court order.

What is a balloon payment trap?

A balloon payment is a large lump sum due at the end of a loan term. Predatory lenders use this to make weekly payments look low. Borrowers often don’t realize they will owe thousands of dollars at the end, forcing them to refinance the balloon payment at high interest rates.