Feeling overwhelmed by debt? You’re not alone. Millions of people grapple with various forms of debt, from credit cards to student loans and mortgages. The path to financial freedom often begins with clarity, and that’s precisely what a powerful debt calculator and effective repayment tools can offer.

Our comprehensive suite of resources is designed to demystify your financial obligations, empowering you to make informed decisions. Whether you’re aiming to understand your current debt load, explore accelerated repayment strategies, or simply visualize your journey to becoming debt-free, this page is your essential guide. Let’s transform uncertainty into a clear, actionable plan.

Table of Contents

How to Use a Debt Calculator Effectively

A debt calculator is more than just a tool; it’s a strategic partner in your financial journey. By inputting key details, you can gain profound insights into your repayment timeline and total costs. Follow these steps to maximize its potential:

1. Gather Your Debt Information

Before you start, collect all necessary details for each debt. This typically includes the principal balance, interest rate (APR), minimum monthly payment, and original loan term (if applicable). The more accurate your data, the more precise the calculator’s output will be.

2. Input Data into the Calculator

Enter the gathered information into the respective fields of the debt calculator. If you have multiple debts, many advanced tools allow you to list them separately to see an aggregated view of your financial situation.

3. Analyze the Repayment Schedule

Once you’ve entered your data, the debt calculator will generate an amortization schedule. This schedule breaks down each payment into principal and interest, showing you how your balance decreases over time. Pay close attention to the estimated payoff date and total interest paid.

4. Experiment with Different Scenarios

This is where the power of the debt calculator truly shines. Adjust your potential monthly payment upwards, or consider making extra payments. See how these changes drastically reduce your payoff time and the overall interest you’ll pay. This interactive exploration helps you visualize the impact of your financial choices.

Understanding Principal and Interest Payments

A fundamental concept in debt management is distinguishing between principal and interest. When you make a loan payment, a portion goes towards reducing the original amount borrowed (the principal), and another portion goes towards the cost of borrowing money (the interest).

Stat Callout:

Historically, interest payments can account for a significant portion of early loan repayments. For example, on a typical 30-year mortgage, over 50% of the initial payments often go towards interest alone. Understanding this dynamic is crucial for strategic repayment.

Early in a loan’s life, a larger percentage of your payment typically covers interest. As you continue to make payments and reduce the principal, a greater portion of each subsequent payment is applied to the principal. This is why making extra payments, especially early on, can have such a dramatic impact – it directly reduces the principal, thereby reducing the amount on which interest is calculated for the remainder of the loan term.

“Understanding the principal-interest split is the cornerstone of effective debt management. It reveals the true cost of borrowing and illuminates the most impactful ways to accelerate your path to debt freedom.”

Strategies for Accelerating Debt Repayment

Armed with your debt calculator insights, it’s time to implement strategies that actively reduce your debt faster. Here are proven methods:

Action Checklist for Faster Debt Payoff:

- Make Extra Payments: Even small additional payments can significantly cut down your repayment time and total interest. Use your debt calculator to see the impact of adding just $25 or $50 to your monthly payment.

- Debt Snowball Method: Pay off your smallest debt first while making minimum payments on others. Once the smallest is paid, roll that payment amount into the next smallest debt. The psychological wins keep you motivated.

- Debt Avalanche Method: Focus on paying off debts with the highest interest rates first. This method saves you the most money on interest in the long run. Use your debt calculator to compare this strategy against the snowball method.

- Refinance High-Interest Debt: If you have good credit, consider refinancing high-interest personal loans or credit card debt into a lower-interest loan.

- Increase Income: Explore opportunities for side hustles, overtime, or negotiating a raise to free up more funds for debt repayment.

- Reduce Spending: Create a strict budget and identify areas where you can cut back, directing those savings towards your debt.

- Consider Debt Consolidation: For multiple high-interest debts, a single consolidation loan can simplify payments and potentially lower your overall interest rate. Be cautious of fees.

Choosing the right strategy depends on your personality and financial situation. Some prefer the quick wins of the snowball method, while others prioritize the maximum savings of the avalanche method. Our debt calculator allows you to model both approaches to see which one resonates best with your goals.

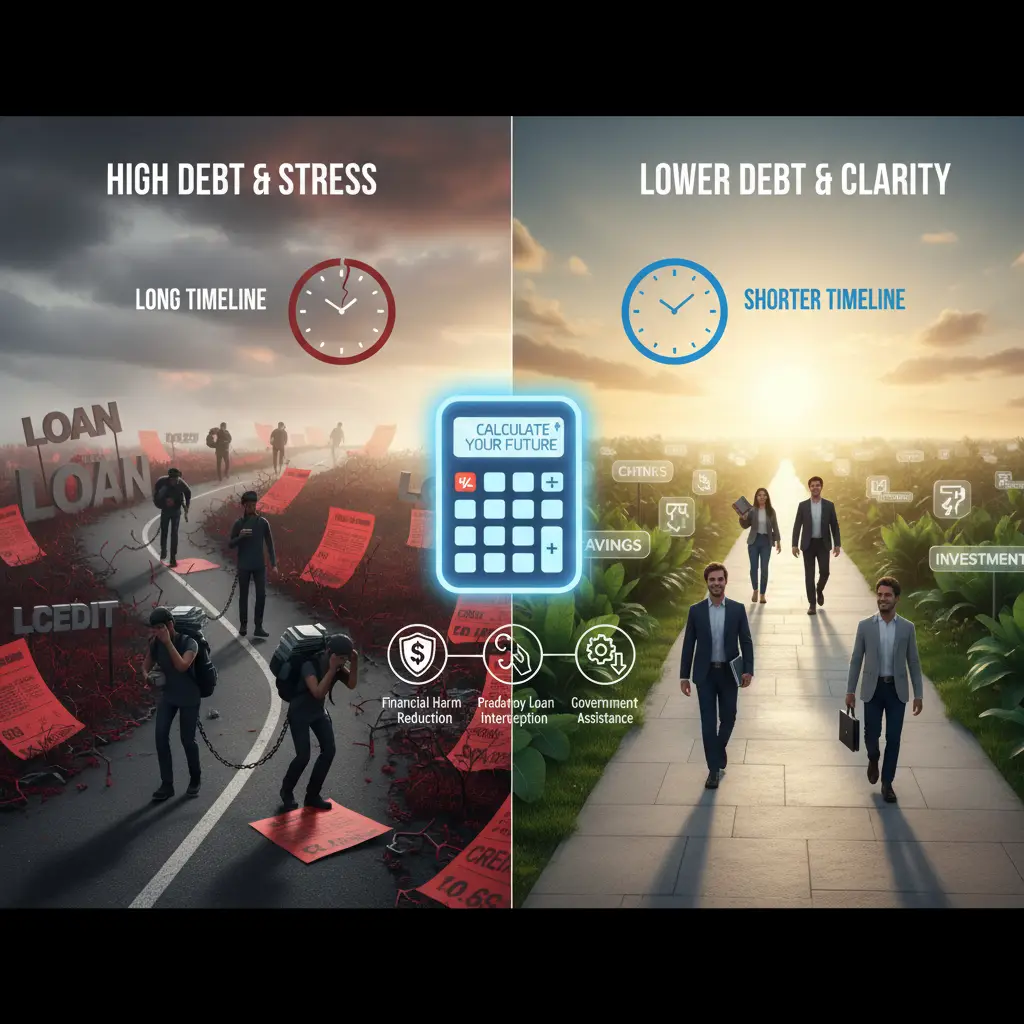

Scenario Planning for Different Repayment Options

Effective financial planning isn’t about rigid adherence; it’s about adaptability. Our debt calculator allows you to engage in powerful scenario planning, helping you visualize the outcomes of various choices before you commit to them.

Imagine you have an unexpected bonus or a tax refund. What if you put that extra money towards your credit card debt, your student loans, or your mortgage? With a debt calculator, you can instantly see how much faster you’d become debt-free and how much interest you’d save in each scenario. This foresight is invaluable for making the most impactful financial decisions.

- “What if I increase my monthly payment by X amount?” See how an extra $50 or $100 per month can shave years off your repayment.

- “What if I pay off my smallest debt first?” Model the debt snowball and see the psychological boost and initial payoff dates.

- “What if I focus on the highest interest rate debt?” Model the debt avalanche and calculate your maximum interest savings.

- “How would a debt consolidation loan impact my monthly payment and total interest?” Compare your current situation to a hypothetical consolidated loan.

By using the debt calculator for scenario planning, you transform abstract financial concepts into concrete, understandable outcomes. This proactive approach ensures you’re always making the smartest moves for your unique financial situation, steering clear of predatory lenders, and leveraging available government assistance and robust debt management strategies.

Frequently Asked Questions

What is a debt calculator and how does it work?

A debt calculator is an online tool that helps you estimate how long it will take to pay off your debts and the total interest you’ll pay, based on your current balance, interest rate, and monthly payments. You input these figures, and the calculator provides a detailed amortization schedule.

What information do I need to use a debt calculator?

You typically need the current balance for each debt, its annual interest rate (APR), and your current or desired monthly payment. For some loans, the original loan term might also be helpful.

Can a debt calculator help me choose a repayment strategy?

Absolutely! By allowing you to adjust payment amounts and see the impact on payoff timelines and total interest, a debt calculator is excellent for comparing strategies like the debt snowball or debt avalanche methods.

Is a debt calculator only for large debts?

No, a debt calculator is useful for any size of debt, from small credit card balances to large mortgages. It provides valuable insights regardless of the amount owed, helping you manage all your financial obligations.

How often should I use a debt calculator?

It’s advisable to use a debt calculator whenever your financial situation changes (e.g., increased income, new debt, interest rate changes) or at least once a quarter to re-evaluate your progress and adjust your repayment plan if necessary.

What’s the difference between principal and interest?

The principal is the original amount of money you borrowed. Interest is the cost you pay to borrow that money. Each payment you make is split between reducing the principal and covering the interest charges.

Can I use a debt calculator for multiple debts?

Many advanced debt calculators allow you to input multiple debts, providing a consolidated view of your overall debt situation and helping you prioritize repayment strategies across all your obligations.

How does a debt calculator help with financial planning?

By offering clear projections of payoff dates and total costs, a debt calculator enables you to set realistic financial goals, allocate funds effectively, and make informed decisions that align with your long-term financial health and freedom.

References

- The National Consumer Law Center. (n.d.). Debt Collection & Debt Buyers. Retrieved from NCLC.org

- Federal Trade Commission. (n.d.). Coping with Debt. Retrieved from FTC.gov

- Consumer Financial Protection Bureau. (n.d.). Understanding Loan Amortization. Retrieved from ConsumerFinance.gov

- American Institute of Certified Public Accountants. (n.d.). Financial Planning: Debt Management. Retrieved from AICPA.org